What Is a Personal Financial Assessment?

A personal financial assessment scores your income, debt, savings, and cash flow from 0 to 100 so you know exactly what to fix first. Here is how to run one.

TL;DR:

- A personal financial assessment provides a clear score of your financial health by analyzing key metrics. It helps identify risks and opportunities, guiding targeted actions for improvement. Regular reviews and professional support ensure your financial progress stays on track and adapts to life changes.

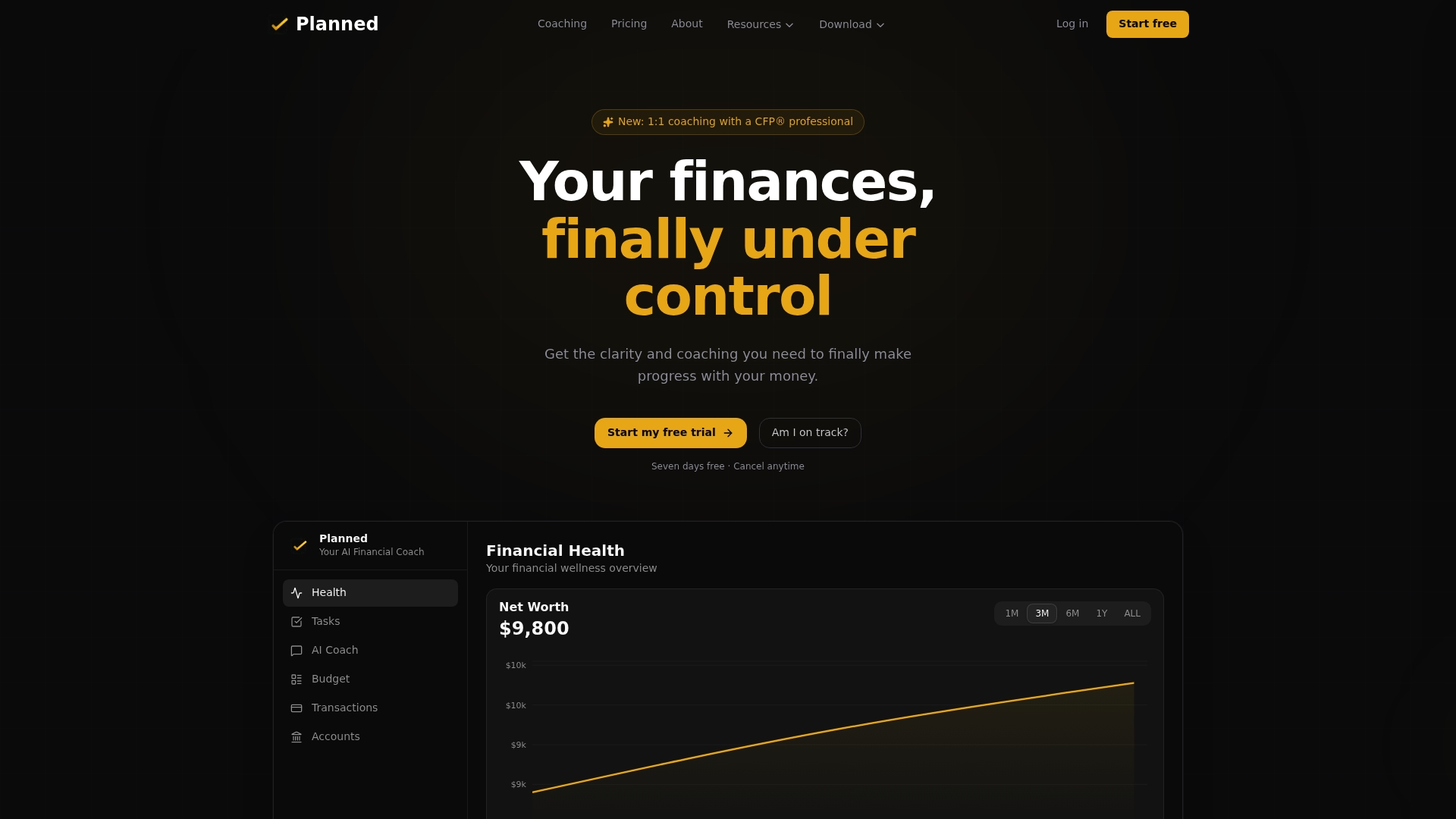

A personal financial assessment is a structured evaluation of your income, expenses, assets, liabilities, and goals that produces a measurable financial health score from 0 to 100. The score tells you exactly where your finances are strong, where they are fragile, and what to fix first. Most people skip it because it feels intimidating, but it only takes 10–30 minutes and gives you a clearer picture of your money than years of vague worrying ever could. Planned’s Financial Health Score feature is built on this same framework, connecting directly to your real accounts so the picture is always accurate.

What is a personal financial assessment and how is it scored?

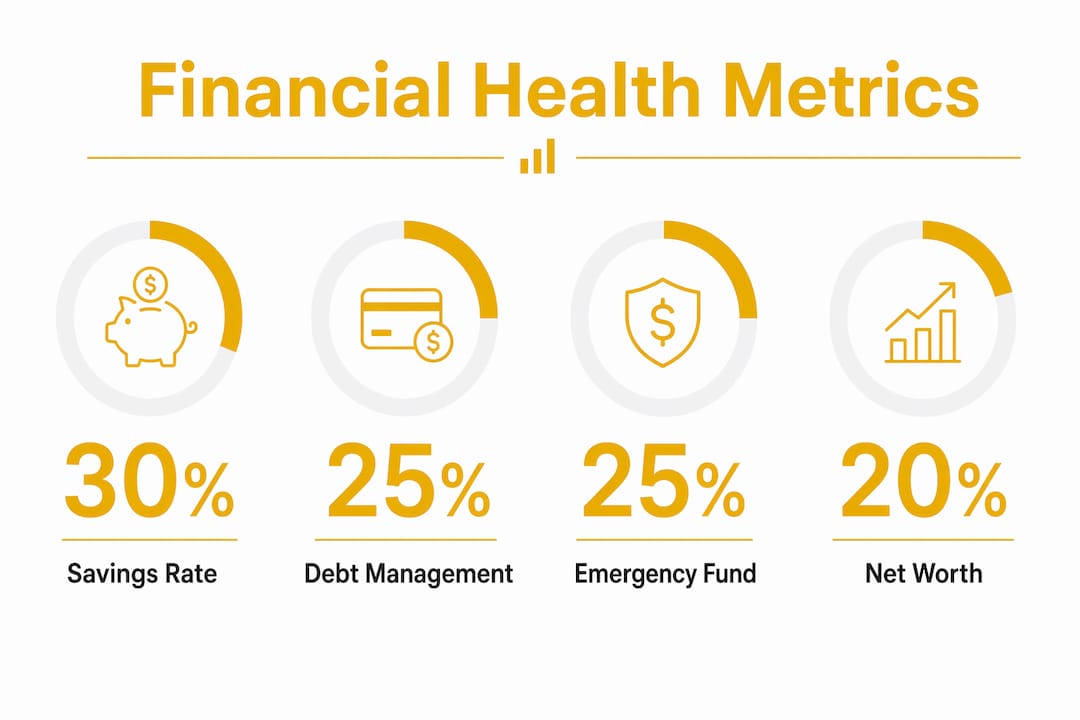

A personal financial assessment is a structured financial review that weights four key metrics: savings rate (30%), debt-to-income ratio (25%), emergency fund coverage (25%), and monthly cash flow (20%). Each category contributes to a final score between 0 and 100. A score of 80 or above signals strong financial discipline. A score below 60 means adjustments are needed before small problems become serious ones.

The scoring framework matters because it removes guesswork. Instead of asking “Am I doing okay with money?” you ask “Is my savings rate above 15%?” That shift from vague to specific is what makes a financial health check genuinely useful. You can read more about interpreting your results in Planned’s guide on reading your financial health report.

Financial health scores typically grade across five categories: emergency fund, debt management, savings rate, net worth relative to income, and retirement readiness. Some frameworks add insurance coverage as a bonus factor. Each category scores up to 20 points, and the total caps at 100. That structure means you can see at a glance which category is dragging your score down and prioritize accordingly.

What are the key elements of conducting a personal financial assessment?

A complete personal finance evaluation requires 12 months of financial records, including pay statements, utility bills, debt balances, and fund account totals. A single month of data is not enough. One month misses annual insurance premiums, car repairs, holiday spending, and other irregular costs that can throw your budget off by hundreds of dollars.

The four metrics you calculate from that data are:

- Savings rate: Your monthly savings divided by gross income. The average American saves 4–5% of income. The recommended savings target is 15–20%.

- Debt-to-income (DTI) ratio: Total monthly debt payments divided by gross monthly income. Lenders prefer DTI under 36%, but a ratio below 20–25% gives you real flexibility.

- Emergency fund coverage: Months of essential expenses covered by liquid savings. Only count funds you can access immediately. Retirement accounts and brokerage holdings do not count here.

- Monthly cash flow: Income minus all expenses. Positive cash flow is good, but it does not guarantee financial health on its own.

Pro Tip: Review at least 12 months of bank and credit card statements before calculating any metric. Irregular expenses like annual subscriptions, car registration, and seasonal utility spikes are easy to miss in a shorter window, and missing them makes your budget look healthier than it actually is.

Distinguishing liquid assets from long-term investments is one of the most common mistakes in a personal budget assessment. A retirement account balance looks reassuring on paper, but you cannot tap it without penalties in a true emergency. Liquid assets only belong in your emergency fund calculation.

How does a financial assessment help identify risks and opportunities?

A financial health check does more than confirm what you already suspect. It surfaces hidden risks that feel invisible when you are managing month to month. The four most common risk signals a personal finance evaluation reveals are:

- Emergency fund gap. Fewer than three months of liquid savings means one job loss or medical bill could force you into debt immediately.

- Credit card reliance. Positive cash flow paired with credit card use for essentials is a warning sign, not a green light. It means your real spending exceeds your real income.

- High DTI ratio. A ratio above 36% leaves almost no room to absorb a rate increase, a car repair, or a reduction in hours at work.

- Savings rate below 10%. At this level, retirement readiness and goal funding both fall behind, often without the person realizing it until years later.

A positive cash flow without an emergency fund is a false signal of financial health. True financial wellness requires looking at qualitative behavior patterns, not just the numbers on a spreadsheet.

The opportunity side of an assessment is equally important. A score below 60 in one category while scoring well in others tells you exactly where to direct your next dollar. That kind of targeted focus beats general advice like “spend less” every time. You can build a stronger safety net by reviewing Planned’s guidance on emergency fund coverage alongside your assessment results.

What best practices make financial assessments accurate and effective?

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Conducting a financial assessment once and never returning to it is the most common mistake people make. Experts recommend reviewing your finances at least annually and after any major life change, including a new job, a marriage, a child, or a significant purchase. Life changes shift your income, expenses, and goals simultaneously, and your benchmarks need to shift with them.

Effective assessment habits share a few consistent traits:

- Use objective benchmarks. The 50/30/20 rule (50% needs, 30% wants, 20% savings and debt) is a widely used starting framework. Adjust it as your goals evolve, but always anchor to a number rather than a feeling.

- Include every expense category. Subscriptions, pet costs, gifts, and personal care are real budget items. Leaving them out produces a flattering but inaccurate picture.

- Separate assessment from judgment. A low score is data, not a verdict. The goal is to see clearly, not to feel bad.

- Set a recurring calendar reminder. Treating your annual review like a scheduled appointment makes it a habit instead of a chore.

Pro Tip: After a major life change, run a quick mid-year check even if your annual review is months away. A new salary, a new rent payment, or a new loan changes every ratio in your assessment. Catching the shift early prevents months of drift in the wrong direction.

Adjusting benchmarks over time is not a sign of lowering your standards. It is a sign of honest planning. A 25-year-old renting an apartment and a 40-year-old with a mortgage and two kids need different targets. Static financial views prevent the kind of long-term changes that actually build wealth.

How do you apply assessment results to improve your financial health?

Assessment results are only useful if they lead to a specific next step. The table below maps common score patterns to the most effective corrective actions.

| Score pattern | What it signals | Best first step |

|---|---|---|

| Low savings rate score | Spending absorbs too much income | Automate a fixed transfer to savings on payday |

| High DTI score | Debt payments limit flexibility | Focus extra payments on the highest-interest debt first |

| Low emergency fund score | Vulnerable to unexpected costs | Build to one month of expenses before other goals |

| Low cash flow score | Monthly deficit or near-zero surplus | Audit subscriptions and discretionary spending for cuts |

| Strong across all categories | On track, ready to grow | Increase retirement contributions or start investing |

When your score is low across multiple categories, prioritize in this order: stop the bleeding (eliminate deficit spending), build a buffer (one month of emergency savings), then attack high-interest debt. Trying to fix everything at once usually results in fixing nothing.

Setting SMART goals directly from your assessment results keeps progress measurable. “Save more money” is not a goal. “Increase my savings rate from 6% to 12% by December 31 by redirecting $300 per month from dining and subscriptions” is a goal you can track. Planned’s AI coach connects to your actual accounts and helps you set targets based on your real numbers, not generic templates.

When a score stays below 60 despite consistent effort, professional help accelerates progress. A CFP® professional or a nonprofit credit counselor can identify structural issues that a self-assessment might miss. The financial advice gaps that most people carry into their 30s and 40s are almost always addressable with the right guidance.

Key Takeaways

A personal financial assessment is the most direct way to replace financial anxiety with a clear, scored picture of where you stand and what to do next.

| Point | Details |

|---|---|

| Assessment produces a scored result | Financial health scores weight savings rate, DTI, emergency coverage, and cash flow across a 0–100 scale. |

| Use 12 months of data | Single-month snapshots miss irregular expenses and produce inaccurate budgets. |

| Positive cash flow is not enough | Credit card reliance for essentials signals a real deficit even when monthly numbers look positive. |

| Review annually and after life changes | Major events shift every ratio; waiting for the next scheduled review causes months of undetected drift. |

| Low scores point to specific fixes | Each category score directs you to one corrective action rather than vague general advice. |

Financial assessments changed how I think about money worry

I spent years treating financial anxiety as a personality flaw rather than a data problem. The turning point was realizing that worry without numbers is just noise. When I started running structured assessments, the anxiety did not disappear, but it became specific. Instead of a general dread about money, I had a DTI ratio that was too high and a savings rate that was too low. Those are solvable problems.

The medical checkup analogy is the most useful reframe I know. You do not skip a physical because you are afraid of bad news. You go because knowing is better than not knowing, and early detection changes outcomes. A financial anxiety management approach that uses objective benchmarks works the same way. The score replaces the spiral.

The other thing I have learned is that starting simple beats waiting until you feel ready. A rough assessment with incomplete data is still more useful than no assessment at all. You can refine the inputs over time. What you cannot do is improve something you have never measured. Run the numbers once, even imperfectly, and you will understand your finances better than most people around you ever will.

— Matt Schuberg

Planned makes your financial assessment work for you

Getting a clear financial health check is one thing. Knowing what to do with the results is another. Planned connects your real financial accounts to an AI coach that reads your actual income, spending, and goals, then gives you specific guidance based on what it finds.

For readers who want expert support alongside the technology, Planned offers 1:1 coaching with a CFP® professional who can walk through your assessment results, identify blind spots, and build a plan that fits your actual life. This is not generic advice. It is guidance built around your numbers. Visit Planned’s financial coaching page to learn how personalized coaching turns assessment results into real progress.

FAQ

What is a personal financial assessment?

A personal financial assessment is a structured review of your income, expenses, assets, liabilities, and goals that produces a financial health score from 0 to 100. It identifies strengths and weaknesses across savings rate, debt-to-income ratio, emergency fund coverage, and monthly cash flow.

How often should I conduct a financial assessment?

Conduct a full assessment at least once a year and after any major life change such as a new job, marriage, or large purchase. Mid-year check-ins after significant changes prevent months of undetected financial drift.

What data do I need to assess my finances?

You need 12 months of financial records including pay statements, utility bills, debt balances, and savings account totals. Reviewing a full year captures irregular expenses like annual insurance premiums and seasonal costs that a single month misses.

What does a financial health score below 60 mean?

A score below 60 signals that one or more key areas, such as savings rate, emergency fund, or debt load, need adjustment before they create serious financial instability. The score pinpoints which category to address first rather than requiring a complete financial overhaul.

When should I get professional financial help?

Seek professional help when your score stays below 60 despite consistent effort, or when your financial situation involves complex decisions like tax planning, estate planning, or significant debt restructuring. A CFP® professional or nonprofit credit counselor can identify structural issues a self-assessment may not surface.

Recommended

CFP® Professional vs. Robo-Advisor: How to Choose

CFP® professional vs robo-advisor: robos run your investments for about 0.25% a year; a CFP® professional plans your whole financial life. How to choose.

The Best Fin100X.AI Alternatives for U.S. Users in 2026

Fin100X.AI is an India-only public-sector platform. Here are 11 U.S. AI alternatives for portfolio monitoring and support automation, compared.

What Is Adaptive Financial Guidance and Why It Matters

Adaptive financial guidance updates your plan as your income, spending, and goals change. Here’s how it works and why it beats static, once-a-year advice.

Ways to Benchmark Your Finances: A Practical Guide

Benchmark your finances with six metrics: emergency fund, debt-to-income, savings rate, housing, consumer debt, and investments. See where you stand today.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?