Ways to Benchmark Your Finances: A Practical Guide

Discover effective ways to benchmark your finances. Learn key metrics to track, gather clean data, and improve your financial health.

Ways to Benchmark Your Finances: A Practical Guide

TL;DR:

- Financial benchmarking involves comparing key personal finance metrics to standards to evaluate your financial health. Most people overlook this step, which can cause feelings of being stuck despite income growth. Focusing on one or two weak metrics first helps guide effective financial improvements.

Financial benchmarking is defined as measuring key personal finance metrics against established standards to understand where you stand and what to fix first. Most people skip this step entirely, which is why they feel stuck even when their income grows. The good news: you do not need a financial degree to do it well. Learning the right ways to benchmark your finances gives you a clear picture of your strengths, your gaps, and your next move. This guide walks you through the exact metrics to track, how to gather clean data, and how to read your results without spiraling into anxiety.

What are the key financial benchmarks you should track?

Financial benchmarking covers six core metrics. Each one tells a different part of your financial story, and together they give you a complete picture of your financial health.

-

Emergency fund coverage ratio. Divide your liquid savings by your monthly essential expenses. Financial guidelines recommend covering 3–6 months of essential living expenses, including housing, utilities, and debt payments. If your ratio falls below 3, building this fund is your first priority.

-

Debt-to-income ratio (DTI). Divide your total monthly debt payments by your gross monthly income. Industry standards suggest keeping DTI at or below 36%. A DTI above 43% signals high financial stress and can block loan approvals. A DTI of 15–28% is considered manageable for someone carrying a mortgage.

-

Savings rate. Divide your monthly savings by your gross income. Financial experts recommend a savings rate of 10–15% as a solid baseline, with 20% or more considered excellent for wealth-building or early retirement. Savings rates of 1–5% are generally not enough to build lasting wealth.

-

Housing cost ratio. Divide your monthly housing costs by your gross monthly income. The widely cited guideline is to keep housing below 28–30% of gross income. Exceeding this threshold regularly crowds out savings and debt repayment.

-

Consumer debt ratio. Divide your non-mortgage debt payments by your net monthly income. Keeping this below 15% leaves room for savings and unexpected costs.

-

Investment assets to net worth ratio. Divide your investment account balances by your total net worth. A higher ratio signals that your wealth is growing, not just sitting in a checking account. You can use a net worth calculator with age benchmarks to see how your ratio compares to typical ranges for your age group.

Pro Tip: Do not try to fix every metric at once. Benchmarks work best as conversation starters, not report cards. Identify your one or two weakest numbers and focus there first.

How do you collect and organize your financial data accurately?

Accurate data is the foundation of any useful financial assessment. If your numbers are incomplete or inconsistent, your benchmarks will mislead you rather than guide you.

-

List every income source. Include your salary, freelance income, side income, and any government benefits. Use your net take-home pay for expense comparisons and your gross income for savings rate and DTI calculations.

-

Track all monthly expenses, including irregular ones. This is where most people go wrong. Ignoring irregular expenses like annual insurance premiums, car registration, or holiday spending can destabilize your budget and skew your benchmarks. Divide annual irregular costs by 12 and add that monthly average to your expense total.

-

Use a consistent timeframe. Compare monthly figures to monthly figures, and annual to annual. Successful benchmarking requires apples-to-apples comparisons using consistent timeframes, ideally averaged over multiple months to smooth out one-time anomalies. A single unusual month, like a medical bill or a bonus, can distort your picture.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

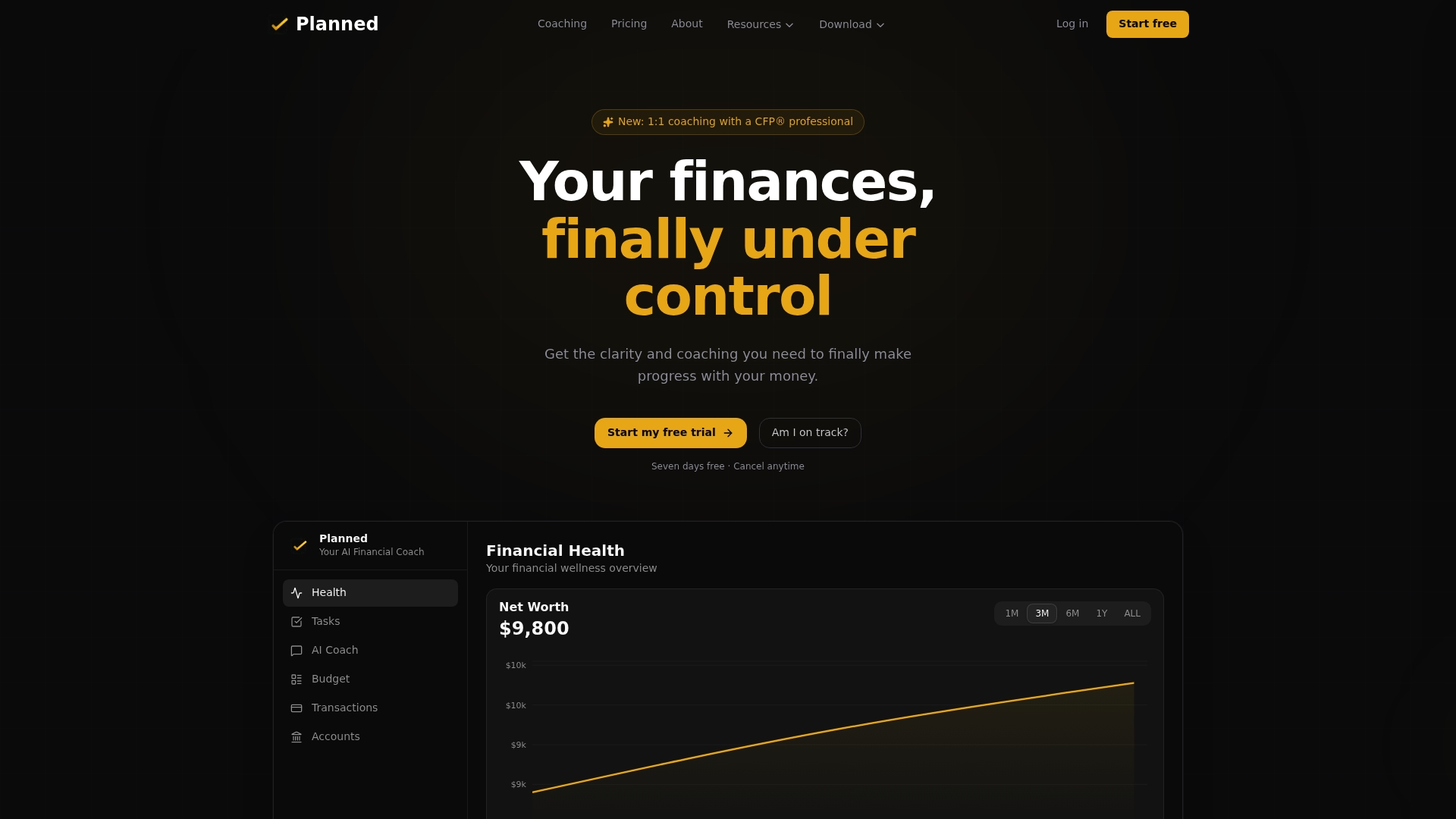

Organize your data in one place. A spreadsheet works well for most people. Apps connected to your real accounts remove the manual entry step and reduce errors. Planned, for example, connects directly to your financial accounts and surfaces your actual spending patterns, so your data is always current.

Verify your numbers before calculating. Cross-check your bank statements against your expense list. Missing a subscription or underestimating groceries by $200 a month adds up to $2,400 a year in untracked spending.

Pro Tip: A practical financial health assessment starts by comparing your monthly take-home income to your total monthly expenses, including irregular costs. That single comparison tells you immediately whether your budget is stable, tight, or negative.

How do you analyze your benchmarks and compare them to standards?

Calculating your numbers is only half the work. Knowing what they mean is where the real value lives.

The table below shows common benchmark ranges and what each zone signals:

| Metric | Healthy range | Warning zone | Action needed |

|---|---|---|---|

| Emergency fund | 3–6 months of expenses | 1–2 months | Below 1 month |

| Debt-to-income ratio | Below 36% | 36–43% | Above 43% |

| Savings rate | 10–15% or higher | 5–9% | Below 5% |

| Housing cost ratio | Below 28% | 28–35% | Above 35% |

| Consumer debt ratio | Below 15% | 15–20% | Above 20% |

Reading these ranges in isolation is a mistake. A person with a strong savings rate but a DTI above 43% is not in good shape overall. Credit scores account for only about 12.5% of a total financial wellness score, which shows that no single metric tells the whole story. Measuring multiple dimensions gives a fuller, more accurate picture of where you actually stand.

Avoid what financial analysts call “benchmarking tunnel vision.” Achieving a strong number in one area can mask serious problems in others. A high savings rate means little if your emergency fund is empty and your consumer debt ratio is climbing.

When you spot a gap, treat it as a signal, not a verdict. Benchmarks are directional data points that inform your next manageable step. If your DTI is above 43%, that becomes your top priority. You do not need to stress about your investment ratio until your debt load is under control. Prioritizing one metric at a time keeps the process from feeling paralyzing.

Age-based context also matters. A 25-year-old with a low investment-to-net-worth ratio is in a very different position than a 45-year-old with the same number. Use personal finance dashboard tools to layer in age-appropriate benchmarks alongside the standard ranges.

Common mistakes that undermine your financial benchmarking habit

Even people who start benchmarking well tend to drift off track. These are the patterns that most often derail a solid financial assessment practice.

-

Skipping irregular expenses. Annual costs like car maintenance, medical copays, and holiday gifts are real expenses. Leaving them out makes your budget look healthier than it is and leads to surprise cash flow problems every few months.

-

Benchmarking once and forgetting it. Your financial situation changes. A raise, a new loan, or a move all shift your ratios. Schedule a full review every three to six months, and do a quick check monthly.

-

Fixating on one metric. A low DTI feels great until you realize your savings rate has been at 2% for three years. Habits around saving and spending often weigh more in comprehensive assessments than any single ratio. Keep all six metrics in view.

-

Using inconsistent data periods. Comparing one month’s expenses to a full year’s income produces meaningless results. Stick to the same timeframe across every metric, every time.

-

Not adjusting goals as life changes. A benchmark that made sense when you were renting may not apply after buying a home. Revisit your personal targets whenever a major life event shifts your income, expenses, or goals.

-

Avoiding professional input. Benchmarks tell you what is happening. A financial professional helps you understand why and what to do about it. If your numbers have been in the warning zone for more than six months, that is a clear sign to get a second set of eyes on your plan. You can also explore credit-related guidance to understand how credit fits into your broader financial picture.

Benchmarking is a compass, not a report card

By Matt Schuberg

The biggest mistake I see people make with financial benchmarking is treating it like a test they can fail. They calculate their DTI, see it is above 36%, and feel defeated before they have done anything useful with the information.

Here is what I have learned after years of working through personal finance frameworks: a benchmark is a compass reading, not a grade. It tells you which direction you are drifting, not whether you are a good or bad person with money. The moment you shift that mindset, benchmarking stops feeling like punishment and starts feeling like a tool you actually want to use.

Start with just two metrics. Pick the one that worries you most and the one you feel best about. The contrast between them is often more instructive than any single number. Knowing you have a strong emergency fund but a weak savings rate tells you something specific: your safety net is in place, so now you can redirect cash flow toward building wealth.

Life changes your benchmarks constantly. A new job, a baby, or a cross-country move will shift every ratio you track. The goal is not to hit a number once and declare victory. The goal is to stay oriented so that when life moves, you can adjust quickly and confidently. That is what separates people who feel in control of their money from those who feel controlled by it.

— Matt Schuberg

Planned can help you put your benchmarks to work

Getting your numbers is one thing. Knowing what to do with them is another.

Planned connects directly to your real financial accounts and gives you a Financial Health Score based on your actual income, spending, and goals. Instead of staring at a spreadsheet and guessing what your DTI means for your life, you can ask Planned a specific question and get a tailored answer grounded in your real data. Early adopters report feeling less anxious about money and more confident in their financial decisions. If you are ready to move from calculating benchmarks to acting on them, Planned’s financial coaching pairs you with a CFP® professional who can help you prioritize and build a plan that fits your actual situation. You can also visit the Planned home page to see how the full platform works.

Key takeaways

Effective financial benchmarking means tracking multiple metrics together, using consistent data, and treating each result as a direction to move in rather than a final score.

| Point | Details |

|---|---|

| Track six core metrics | Emergency fund, DTI, savings rate, housing ratio, consumer debt ratio, and investment ratio together give a complete picture. |

| Include irregular expenses | Annual and seasonal costs must be averaged monthly to avoid misleading benchmarks and surprise cash flow gaps. |

| Use consistent timeframes | Compare monthly to monthly and annual to annual; multi-month averages smooth out one-time anomalies. |

| Prioritize one gap at a time | Focus on your weakest metric first; fixing everything at once leads to inaction. |

| Review every 3–6 months | Life changes shift your ratios; regular reviews keep your benchmarks relevant and your goals realistic. |

FAQ

What is financial benchmarking for individuals?

Financial benchmarking is the practice of measuring your personal finance metrics, such as your savings rate, debt-to-income ratio, and emergency fund, against established standards to identify strengths and gaps. It gives you a structured way to evaluate your financial health rather than relying on guesswork.

What is a good debt-to-income ratio?

A DTI at or below 36% of gross income is the widely accepted standard for financial stability. Ratios above 43% are linked to loan approval difficulties and elevated financial stress.

How often should I review my financial benchmarks?

A full review every three to six months is a practical cadence for most people, with a quick monthly check on spending and savings. Major life events like a new job, a move, or a new loan warrant an immediate review.

Why is my savings rate more important than my credit score?

Your savings rate directly determines your ability to build wealth over time, while your credit score reflects past borrowing behavior. Credit scores account for only about 12.5% of a comprehensive financial wellness score, meaning your saving and spending habits carry more weight in your overall financial health.

How do I start benchmarking if my finances feel messy?

Start by comparing your monthly take-home income to your total monthly expenses, including irregular costs. That single comparison tells you whether your budget is stable, tight, or negative, and gives you a clear first priority to address.

Recommended

Financial Baseline Explained: Your Personal Finance Guide

A financial baseline is a fixed snapshot of your past income and spending. Here's how to set yours from 12 months of data and measure real progress each year.

10 Proven Ways to Reduce Financial Stress in 2026

Reduce financial stress in 2026 with 10 proven steps: a 20-minute budget, automated savings, a $500 emergency fund, and a debt payoff method that sticks.

Common Financial Advice Gaps to Fill in 2026

Financial advice gaps are blind spots in risk, taxes, estate, and investing that cost you money. Here's how to spot and fix the five biggest in 2026.

The Role of Financial Education in Calm and Confidence

Financial education lowers money anxiety by replacing uncertainty with clear planning skills. Here's how financial literacy builds real calm and confidence.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?