Financial Baseline Explained: Your Personal Finance Guide

Discover the financial baseline explained. Learn how a financial baseline can help you track your financial health and make informed decisions.

Financial Baseline Explained: Your Personal Finance Guide

TL;DR:

- A financial baseline is a fixed reference point reflecting past income and expenses. It helps measure progress and improve financial clarity over time.

A financial baseline is a fixed, objective historical reference point used to measure current and future financial performance against past results. Think of it as your financial starting line. Without one, you have no reliable way to know whether your spending is improving, your savings are growing, or your income is keeping pace with your goals. Understanding your financial baseline is the first step toward assessing your financial health with real clarity. The Financial Accounting Standards Board (FASB) frames consistent historical comparison as a cornerstone of meaningful financial analysis, and that principle applies just as powerfully to your personal finances as it does to corporate reporting.

Financial baseline explained: what it actually means

A financial baseline is a fixed historical reference point used to compare current or future performance against past results. It tracks metrics like revenue, costs, and profits over time. The key word is fixed. A baseline does not move every time your circumstances shift. It holds steady so you can measure real change.

Here is a concrete example. If your take-home income in 2024 was $48,000 and your total spending was $42,000, those numbers become your baseline. In 2025, you compare everything against that reference point. A $2,000 drop in spending is only meaningful because you have a fixed number to compare it to.

A baseline is not the same as a goal or a budget. A goal is where you want to go. A budget is your plan for getting there. A baseline is simply where you started. Confusing these three concepts is one of the most common mistakes people make when trying to understand their financial health.

How is a financial baseline established and maintained?

Setting a solid baseline takes a few deliberate steps. Skipping any one of them produces a reference point that misleads more than it guides.

- Gather recent, stable data. Pull at least 12 months of income and expense records. Use a period that reflects your normal financial life, not an unusual one.

- Avoid anomalous periods. Selecting anomalous periods like pandemic-affected years skews projections and makes variances unreliable. A year with a large one-time expense or an unexpected job loss distorts your true picture.

- Capture both actuals and forecasts. A functional baseline requires that your current figures and forward projections are up to date before you lock them in. Variance against a baseline is calculated as forecast minus original baseline, so accuracy at the starting point matters.

- Snapshot and commit. Once you set the baseline, treat it as fixed. Changing it casually defeats the purpose.

- Re-baseline only when justified. A major life change, such as a new job, a move, or a significant income shift, may warrant a formal reset. But re-baselining should be rare and controlled. Frequent resets mask prior variances and make long-term tracking meaningless.

Pro Tip: Before snapshotting your baseline, reconcile every account. An unrecorded expense or missed deposit will corrupt your reference point from day one.

Maintaining a baseline is mostly about discipline. Review it quarterly, note any variances, and resist the urge to adjust it just because reality looks different than expected. That tension between baseline and reality is exactly the information you need.

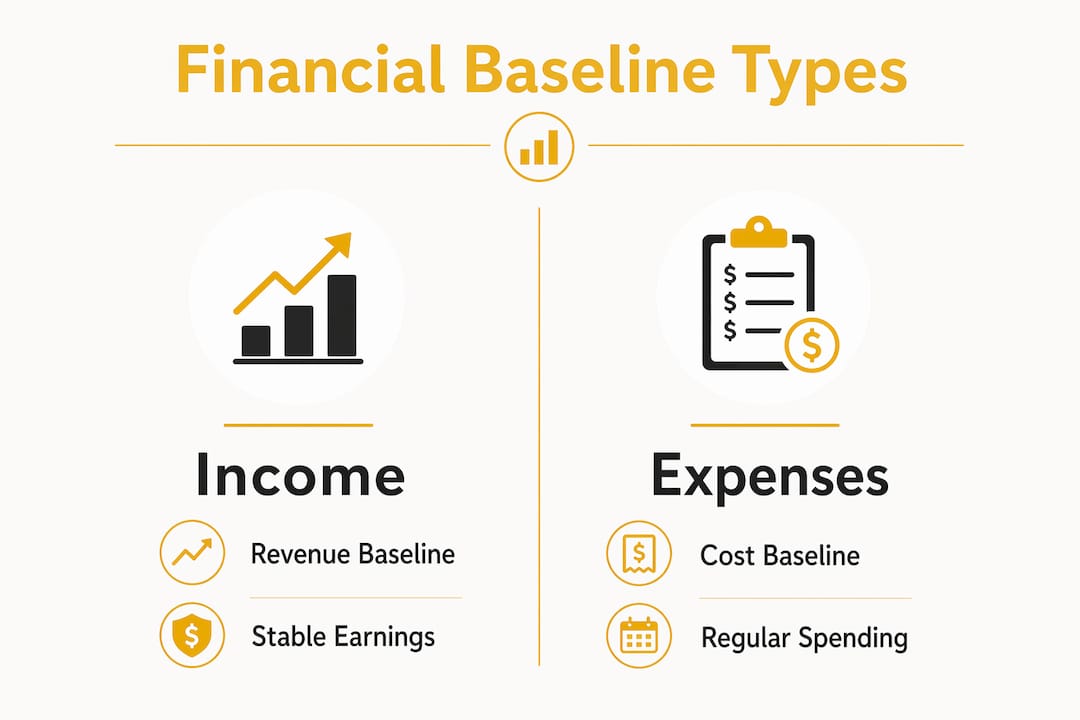

What are the common types of financial baselines?

Not every baseline measures the same thing. Knowing which type applies to your situation helps you use the concept correctly.

- Revenue baseline. This tracks your income over a set period. For individuals, it typically means total take-home pay, freelance earnings, or combined household income. It answers the question: is my income growing, shrinking, or holding steady?

- Cost baseline. In project management, the cost baseline is a time-phased budget showing expected spending across a timeline. For personal finance, it translates to your expected monthly or annual spending by category.

- Operating expense baseline. This focuses specifically on recurring, predictable costs. Rent, utilities, subscriptions, and groceries all belong here. Tracking these separately from irregular expenses gives you a cleaner picture of your fixed financial obligations.

- Project milestone baseline. If you are saving for a specific goal, such as a home down payment or a debt payoff, a milestone baseline sets the timeline and amount benchmarks you measure progress against.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

One distinction worth understanding clearly: a cost baseline is not the same as your total budget. Your total budget includes reserves for unexpected costs. Your cost baseline covers only planned, expected spending. Using the total budget figure as your baseline inflates the reference point and makes your variance analysis meaningless.

| Baseline type | What it measures | Personal finance example |

|---|---|---|

| Revenue baseline | Income over time | Annual take-home pay of $52,000 |

| Cost baseline | Planned spending by category | Monthly groceries budgeted at $400 |

| Operating expense baseline | Fixed recurring costs | Rent + utilities + subscriptions |

| Milestone baseline | Progress toward a goal | $10,000 saved toward a $20,000 down payment |

How does a financial baseline support budgeting and financial health?

A baseline converts raw numbers into context. Without it, your budgeting decisions rest on guesswork rather than evidence.

Here is how the connection works in practice:

- Variance analysis. Compare your actual spending each month against your baseline. A $200 overage in dining out is a signal. A consistent $200 overage for three months is a pattern that demands a response.

- Trend identification. Baselines reveal whether your financial habits are improving or drifting. If your savings rate was 12% in your baseline year and it has dropped to 8%, you know exactly where to focus.

- Realistic goal setting. Goals built on baseline data are grounded in reality. If your baseline shows you typically spend $3,500 per month, a budget that assumes $2,800 will fail. A baseline keeps you honest.

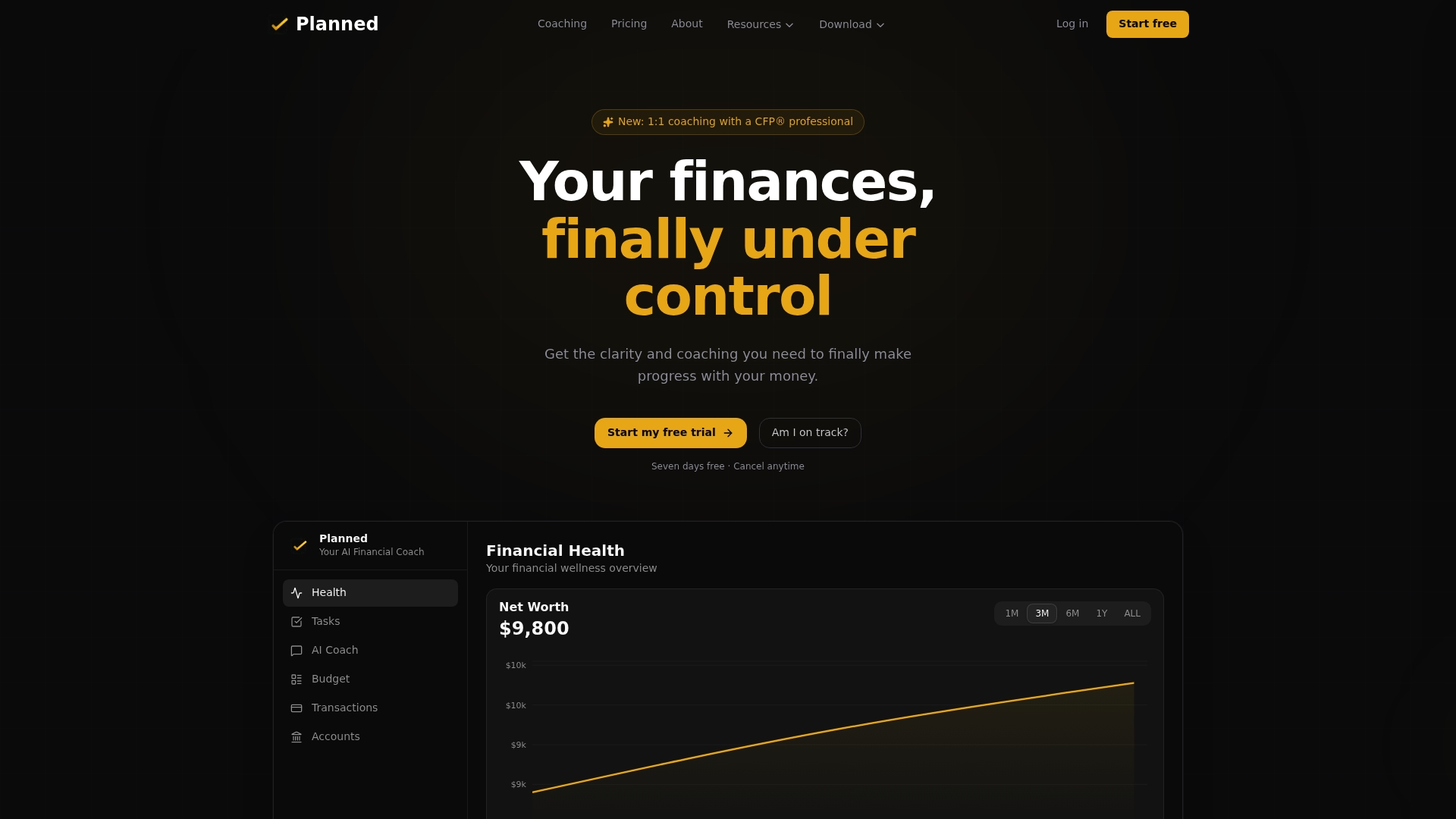

- Financial health assessment. Tools like Planned’s Financial Health Score use your actual account data to measure where you stand relative to your own history, not a generic national average. That personalized comparison is only possible when you have a clear baseline.

Pro Tip: Run a simple variance check at the end of each month. List five spending categories, compare each to your baseline, and write one sentence explaining any gap over $100. This habit builds financial self-awareness faster than any app alone.

Outdated or biased baselines distort conclusions and undermine the quality of your financial assessment. If your baseline year included a large inheritance or an unusually low rent, your comparisons will mislead you. Objectivity in selecting your baseline period is not optional. It is the foundation everything else rests on.

What are the best practices and pitfalls when using financial baselines?

Getting the concept right is one thing. Applying it without common errors is another.

- Do not use outlier years. A year with a major medical expense, a windfall, or a job gap is not representative. It will skew every comparison you make against it.

- Understand the difference between a baseline and a benchmark. A baseline is your own historical data. A benchmark is an external standard, such as the average savings rate for your age group. Both are useful, but they answer different questions.

- Keep your baseline data consistent. If you tracked spending in five categories last year, track the same five this year. Changing your categories mid-stream makes comparison impossible.

- Avoid “rubber-baselining.” This is the practice of quietly adjusting your baseline whenever results look bad. It feels like flexibility, but it destroys the integrity of your tracking over time.

A baseline only works if you protect it. The moment you start adjusting it to match reality, you lose the ability to measure reality. The discomfort of a bad variance is the whole point. It tells you something true.

Financial baselines serve as a bridge between raw numbers and real decisions. When you treat your baseline as an operational tool rather than a compliance checkbox, it reveals inefficiencies you would otherwise miss. That shift in mindset is what separates people who track their finances from people who actually improve them.

When a genuine life change occurs, such as a marriage, a new income source, or a major relocation, a formal re-baseline is appropriate. Planned’s guidance on personalizing your financial plan by income walks through exactly when and how to reset your reference point without losing historical context.

Key Takeaways

A financial baseline is a fixed historical reference point that makes every budgeting decision, variance analysis, and financial health assessment more accurate and meaningful.

| Point | Details |

|---|---|

| Define your baseline clearly | Use 12 months of stable, representative income and spending data as your starting point. |

| Avoid anomalous periods | Never use outlier years like pandemic periods; they distort every comparison that follows. |

| Distinguish baseline from budget | A cost baseline covers planned spending only; your total budget adds reserves on top of that. |

| Use variance analysis monthly | Compare actuals to your baseline each month to catch spending patterns before they compound. |

| Re-baseline rarely and formally | Reset your baseline only after a major life change, and document the reason clearly. |

Why your baseline is the most underused tool in personal finance

Most people I work with arrive with spreadsheets, apps, and good intentions. What they rarely have is a fixed reference point. They know roughly what they spend, but they cannot tell you whether that number is better or worse than last year. That gap is where financial anxiety lives.

The financial baseline concept comes from corporate accounting and project management, where it is treated as non-negotiable. Yet in personal finance, it gets skipped entirely. People jump straight to budgeting without ever establishing what “normal” looks like for them. That is like trying to measure weight loss without ever stepping on a scale at the start.

What I have found is that the act of setting a baseline, even a rough one, changes how people relate to their money. It shifts the conversation from “I think I overspend on food” to “I spent $180 more on food this month than my baseline.” One is a feeling. The other is a fact you can act on. That specificity is what reduces financial anxiety more than any motivational framework.

The misconception I push back on hardest is the idea that baselines are for people with complicated finances. They are not. If you earn a paycheck and pay bills, you have enough data to set a baseline today. The simpler your finances, the faster you will see the baseline pay off in clarity and confidence.

— Matt Schuberg

How Planned helps you put your baseline to work

Setting a baseline is straightforward once you know what you are looking for. Applying it consistently, and knowing what to do when the numbers surprise you, is where most people benefit from guidance.

Planned connects directly to your real financial accounts and gives you a Financial Health Score based on your actual income, spending history, and goals. That score is built on your personal baseline, not a generic average. You can ask Planned’s AI coach specific questions about your numbers and get answers grounded in your real data. For readers who want deeper support, 1:1 coaching with a CFP® professional is available to help you set, interpret, and act on your financial baseline with confidence. Visit Planned to see where you stand today.

FAQ

What is a financial baseline in simple terms?

A financial baseline is a fixed snapshot of your income and spending from a past period, used as a reference point to measure whether your finances are improving or declining over time.

How is a financial baseline different from a budget?

A budget is a forward-looking plan for how you intend to spend money. A financial baseline is a historical record of how you actually spent it, used to make future comparisons meaningful.

How often should you update your financial baseline?

Update your baseline only when a major life change occurs, such as a new job, a move, or a significant income shift. Frequent resets damage the integrity of your long-term performance tracking.

What data do you need to set a personal financial baseline?

You need at least 12 months of income records and categorized spending data from a stable, representative period. Avoid years with large one-time events that do not reflect your normal financial life.

Why does the choice of baseline period matter so much?

A poor baseline period distorts every comparison that follows. Choosing a year with unusual income or expenses makes your variance analysis unreliable and your financial decisions less informed.

Recommended

10 Proven Ways to Reduce Financial Stress in 2026

Discover 10 proven ways to reduce financial stress in 2026. Implement realistic strategies to regain control over your finances today!

Common Financial Advice Gaps to Fill in 2026

Financial advice gaps are blind spots in risk, taxes, estate, and investing that cost you money. Here's how to spot and fix the five biggest in 2026.

The Role of Financial Education in Calm and Confidence

Financial education lowers money anxiety by replacing uncertainty with clear planning skills. Here's how financial literacy builds real calm and confidence.

Top 5 Joinopto.ai Alternatives for 2026

Explore 5 joinopto.ai alternatives to help you decide which AI-driven financial management tool best optimizes your budgeting and saving strategies.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?