Types of Personal Financial Goals: A Complete Guide

Discover the types of personal financial goals you can set to secure your future. Learn how to manage your income, savings, and spending effectively.

Types of Personal Financial Goals: A Complete Guide

TL;DR:

- Personal financial goals are specific, time-bound targets aimed at achieving meaningful outcomes. Organizing goals by time horizon and function helps prioritize saving, protect long-term wealth, and increase motivation.

Personal financial goals are defined as specific, time-bound targets you set to direct your income, saving, and spending toward outcomes that matter to you. The most effective way to organize these goals is by two frameworks: time horizon (short, medium, and long term) and functional purpose (foundation, stability, growth, and aspiration). Understanding the types of personal financial goals you are working toward tells you exactly where to put your money, in what order, and with what level of risk. Without that structure, most people end up reacting to financial stress instead of building toward financial security.

1. Types of personal financial goals: the two core frameworks

Financial goals are classified by time horizon into three tiers: short-term (under one year), medium-term (one to five years), and long-term (over five years). Each tier calls for a different savings vehicle, risk level, and level of urgency. The second framework organizes goals by function: foundation, stability, growth, and aspiration. These two frameworks work together. Time horizon tells you when you need the money. Functional category tells you why you need it and how to protect it.

Using both frameworks prevents a common and costly mistake: raiding your retirement account to cover a car repair because you never built an emergency fund. When your goals are sorted by both time and purpose, each dollar has a clear job.

2. Short-term financial goals: building your foundation

Short-term goals have a timeline of less than one year. They focus on capital preservation and low-risk vehicles like high-yield savings accounts or money market accounts. The priority here is protecting what you have, not growing it.

Common short-term personal finance objectives include:

- Building a starter emergency fund of $1,000 to cover minor unexpected expenses

- Paying off a high-interest credit card to stop interest from compounding against you

- Creating a monthly budget that accounts for all fixed and variable expenses

- Saving for a specific near-term purchase, such as a new laptop or a car repair fund

The SMART framework makes these goals concrete. Instead of “save more money,” a SMART goal reads: “Save $1,800 in six months by depositing $300 per month into a high-yield savings account.” That specificity turns a wish into a plan.

Pro Tip: Complete your short-term foundation goals before putting money toward anything else. Skipping this step means any financial shock, a medical bill, a job loss, a car breakdown, will force you into debt.

3. Medium-term financial goals: stepping stones to bigger wins

Medium-term goals sit in the one-to-five-year range. They balance stability with modest growth, often mixing cash savings with low-to-moderate risk assets. These goals are the bridge between your immediate needs and your long-term aspirations.

Strong examples of medium-term financial goals include:

- Saving a home down payment, typically 10–20% of a target purchase price

- Paying off student loans ahead of schedule to reduce total interest paid

- Building a full emergency fund of three to six months of living expenses

- Funding a career transition, such as saving for a certification program or graduate school

- Creating an opportunity fund for a business idea or investment you want to pursue

Setting measurable milestones matters here. If your goal is a $30,000 down payment in four years, you need to save $625 per month. Knowing that number lets you adjust your monthly budget before you start, not after you fall short.

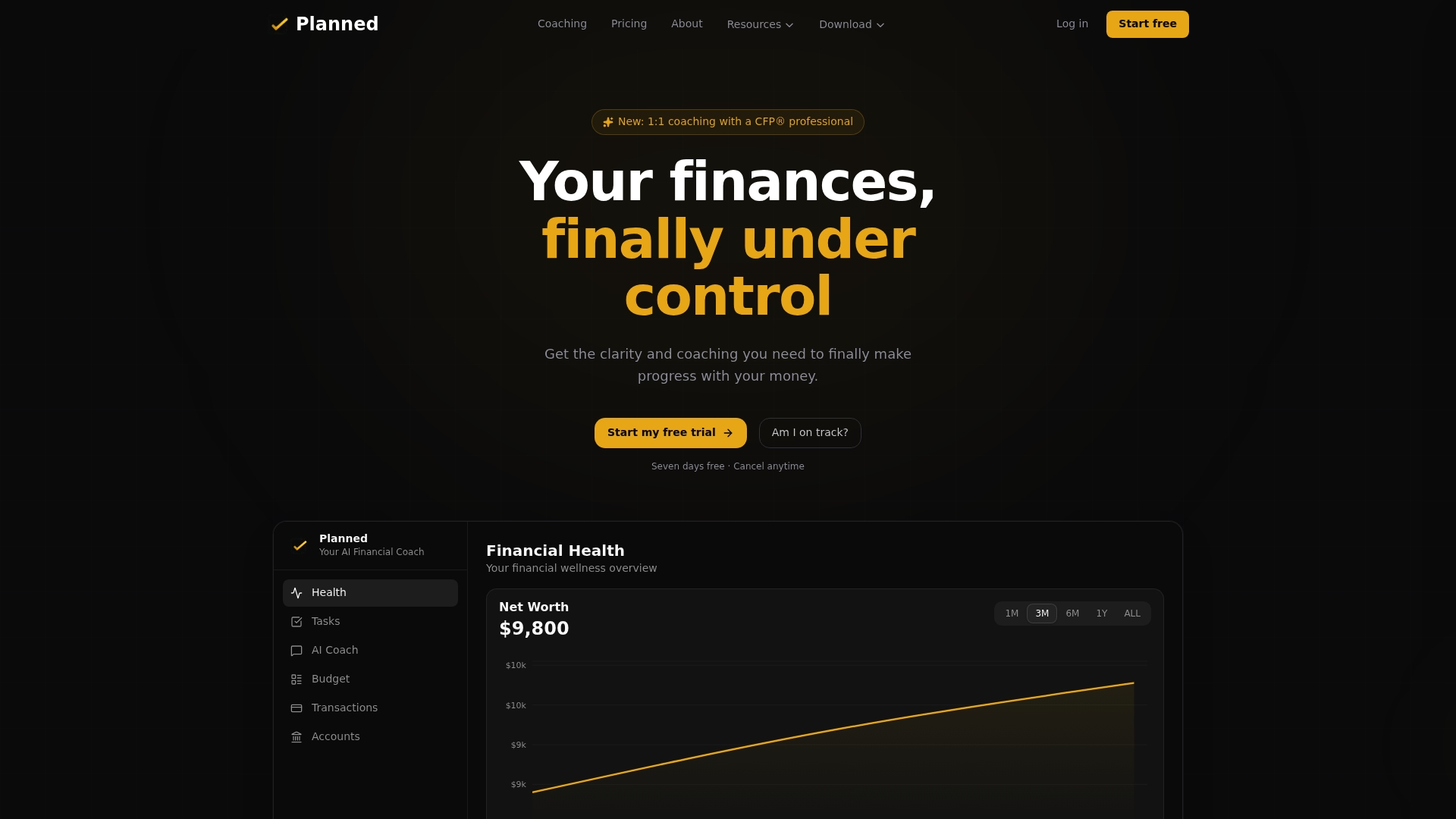

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Pro Tip: When you pay off a debt, redirect that monthly payment amount directly to your next medium-term goal. You were already living without that money, so you will not miss it.

4. Long-term financial goals: building wealth over decades

Long-term goals extend beyond five years, with the most impactful ones stretching ten years or more. These goals use higher-risk assets like equities and index funds to harness compounding growth. Because the timeline is long, short-term market swings matter far less.

Classic long-term financial aspirations include:

- Retirement savings through accounts like a 401(k) or Roth IRA

- Paying off a mortgage to eliminate your largest fixed expense

- Funding a child’s college education through a 529 plan

- Achieving financial independence, where investment income covers living expenses

- Building generational wealth through real estate or a diversified investment portfolio

The SMART framework still applies at this scale. “Retire comfortably” is not a goal. “Accumulate $1,000,000 in retirement accounts by age 65 by contributing $500 per month starting at age 30” is a goal. That level of specificity lets you track progress and adjust when life changes.

Long-term goals also need protection from short-term panic. Keeping these funds in separate, labeled accounts reduces the temptation to tap them during a rough month.

5. Functional goal categories: how to prioritize and protect your finances

The four functional categories, developed as a framework by FemWealth, give every goal a role in your overall financial picture. They are foundation, stability, growth, and aspiration.

| Category | Purpose | Examples |

|---|---|---|

| Foundation | Cash liquidity and emergency protection | Emergency fund, cash reserves |

| Stability | Eliminating debt and reducing financial risk | Paying off high-interest debt, student loans |

| Growth | Long-term wealth building through investing | Retirement accounts, index funds, real estate |

| Aspiration | Named, specific, time-bound personal goals | Dream vacation, home purchase, business launch |

Foundation goals act as infrastructure for everything else. Without cash reserves, any unexpected expense forces you to borrow or pull from growth accounts. Stability goals, particularly eliminating high-interest debt, free up monthly cash flow and prevent new debt from forming. Growth goals build wealth over time and should be left alone to compound. Aspiration goals are the ones that keep you motivated because they are personal and specific.

Pro Tip: Fund your categories in order: foundation first, then stability, then growth, then aspiration. Skipping ahead feels good in the short term but leaves you exposed when something goes wrong.

6. How to set and prioritize your personal financial goals effectively

The most common mistake in personal finance is setting vague goals. The SMART method transforms vague intentions into manageable habits by requiring specificity, measurability, achievability, relevance, and a deadline. Every goal you set should pass all five criteria before you fund it.

A practical approach to setting financial targets:

- List every goal you have, from small to large, without filtering

- Assign each goal a category: foundation, stability, growth, or aspiration

- Assign a time horizon: short, medium, or long term

- Apply the SMART criteria to each goal and rewrite vague ones

- Rank by category, funding foundation goals first, then working up the ladder

- Name each goal with a title that means something to you

Naming goals matters more than most people expect. Naming goals with emotionally resonant titles like “The Freedom Fund” or “First Home Deposit” increases motivation and follow-through. Abstract savings targets are easy to deprioritize. A goal with a name feels real.

Financial goals reflect life stages and should be revisited at least once a year. A job change, a new baby, or a paid-off debt all shift your priorities. When you pay off a loan, redirect that payment toward the next goal on your list. This phased approach keeps momentum going without requiring a raise or a windfall.

Separating needs from wants early in the goal-setting process prevents budget misallocation. Your emergency fund is a need. A vacation is a want. Both are valid goals, but they belong in different categories and get funded in a specific order.

Pro Tip: Use a savings priority calculator to see exactly which goal deserves your next dollar. It removes the guesswork and keeps you from funding aspiration goals before your foundation is solid.

Key takeaways

Organizing personal financial goals by both time horizon and functional category is the single most effective way to prioritize saving, protect long-term wealth, and stay motivated.

| Point | Details |

|---|---|

| Two frameworks matter | Classify every goal by time horizon and functional category for clear prioritization. |

| Fund in order | Build foundation goals first, then stability, growth, and aspiration. |

| SMART goals work | Specific, measurable, time-bound goals are far more likely to be achieved than vague ones. |

| Name your goals | Emotionally resonant goal names increase motivation and follow-through. |

| Revisit annually | Life changes shift priorities; review and adjust your goals at least once a year. |

Why goal categories changed how I think about personal finance

The most damaging financial habit I have seen is not overspending. It is underprioritizing. People set ten goals at once, fund them all a little, and make real progress on none of them. The category framework fixed that for me and for most people I have worked with.

What surprised me most was how much the naming step matters. When a goal is called “retirement savings,” it feels abstract and distant. When it is called “The Day I Stop Answering Emails,” it becomes personal. That emotional connection is not a gimmick. It is a behavioral finance principle that tracking named goals consistently outperforms tracking anonymous savings balances.

The other insight worth sharing: categorizing goals by function protects your long-term goals from being derailed by short-term needs. Without a foundation category, every emergency becomes a retirement problem. With one, your growth accounts stay untouched.

My honest advice is to stop trying to fund everything at once. Pick your foundation goal, name it, set a SMART target, and automate one transfer. That single move puts you ahead of most people who have been “thinking about saving” for years.

— Matt Schuberg

How Planned helps you build and track your financial goals

Getting clear on your financial goals is one thing. Knowing exactly how to fund them, in what order, and with what tools is where most people get stuck.

Planned is a personal financial coaching platform that connects an AI coach directly to your real financial accounts. Instead of generic advice, you get answers based on your actual income, spending, and goals. Planned’s Financial Health Score shows you where you stand right now, and 1:1 coaching with a CFP® professional helps you build a goal plan that fits your life. Early adopters report reduced financial anxiety and stronger confidence in their decisions. Explore Planned’s free financial tools to start organizing your goals today.

FAQ

What are the main types of personal financial goals?

Personal financial goals are classified by time horizon (short, medium, and long term) and by functional category (foundation, stability, growth, and aspiration). Using both frameworks helps you prioritize which goals to fund first and how to protect each one.

What is a short-term financial goal example?

A strong short-term example is saving $1,800 in six months by depositing $300 per month into a high-yield savings account. Short-term goals focus on capital preservation and typically have a timeline of under one year.

How do I prioritize multiple financial goals at once?

Fund foundation goals first (emergency fund), then stability goals (high-interest debt payoff), then growth goals (retirement), and finally aspiration goals (vacation, home). This order protects your long-term wealth from being disrupted by short-term financial shocks.

What is the SMART framework for financial goals?

SMART stands for specific, measurable, achievable, relevant, and time-bound. Applying it turns vague intentions like “save more” into concrete plans like “save $5,000 for a home down payment by december 2026 by saving $417 per month.”

How often should I review my financial goals?

Financial goals should be reviewed at least once a year, or after any major life change such as a new job, a marriage, or a paid-off debt. Redirecting freed-up cash flow toward the next goal keeps your financial plan moving forward.

Recommended

Why Understanding Finances Reduces Fear and Anxiety

Understanding your finances reduces money anxiety by turning vague fears into concrete facts. Learn how financial literacy builds calm at any income level.

What Does Financial Profile Mean? Your 2026 Guide

Discover what a financial profile means and how it shapes your financial health. Learn to make smarter money decisions today!

How to Personalize Your Financial Plan by Income

Personalize your financial plan by income: total your real earnings, match your savings rate to your bracket, and review it quarterly as life changes.

What Is Financial Mental Load and How to Manage It

Financial mental load is the ongoing background effort of managing your money. Learn what it is, who carries it most, and practical ways to reduce it.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?