What Is Adaptive Financial Guidance and Why It Matters

Discover what is adaptive financial guidance and how it provides personalized, real-time advice tailored to your changing life and goals.

What Is Adaptive Financial Guidance and Why It Matters

TL;DR:

- Adaptive financial guidance continuously updates personalized advice based on your behavior, goals, and life changes. It outperforms static advice by using reinforcement learning, behavioral models, and near-real-time data to improve wealth outcomes and reduce anxiety. This approach shifts focus from product-selling to behavior management, providing more responsive and effective financial support.

Adaptive financial guidance is defined as a continuous, personalized approach to financial advice that updates recommendations in real time based on your actual behavior, goals, and changing life circumstances. Unlike a one-time financial plan, it uses technologies like reinforcement learning and behavioral finance principles to keep your guidance current and relevant. The industry also refers to this as dynamic financial planning or continuous financial coaching. Planned, for example, connects an AI coach directly to your real financial accounts so every recommendation reflects your actual income, spending, and goals. If you’ve ever felt like generic financial advice just doesn’t fit your life, this approach was built to fix exactly that.

What is adaptive financial guidance, and how does it differ from traditional advice?

Traditional financial advice is static. You meet with an advisor once or twice a year, get a plan, and then try to follow it until your next appointment. Life changes constantly, but your plan doesn’t.

Adaptive financial guidance works differently. It operates as a continuous feedback loop, observing your financial behavior, recommending adjustments, and refining those recommendations over time. Reinforcement learning algorithms power this process by treating your financial situation like a dynamic environment, not a fixed snapshot. The system watches what you do, measures outcomes, and gets better at guiding you with every cycle.

Here’s what that difference looks like in practice:

- Static advice gives you a savings rate target based on your income at one point in time. If you get a raise, lose a job, or have a baby, the advice stays the same until you go back to your advisor.

- Adaptive guidance detects the change in your cash flow and adjusts your savings recommendations within days, not months.

- Static advice benchmarks your investments against a market index. Adaptive guidance measures your progress against your personal goals, like buying a home or retiring at 60.

- Static advice reacts to problems after they appear. Adaptive guidance flags risks before they become problems.

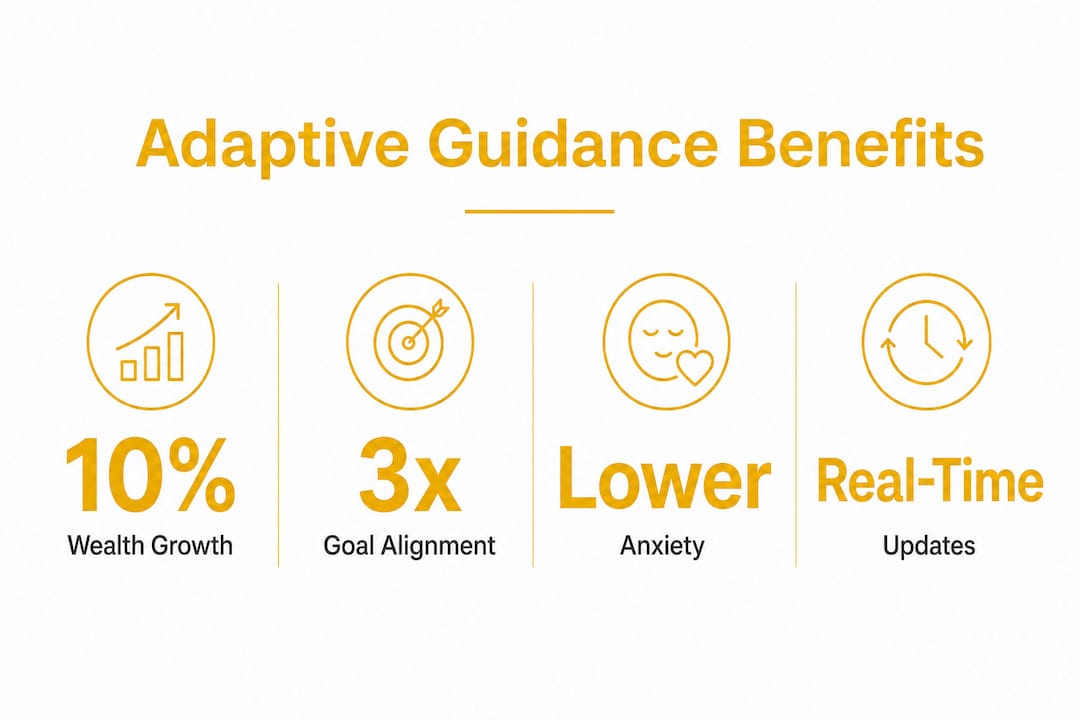

The result is a system that grows with you. Adaptive systems achieve approximately 10% higher net wealth accumulation than traditional static advisory methods. That gap compounds over decades.

Pro Tip: When evaluating any financial guidance tool or service, ask one question: “Does this update when my life changes?” If the answer is no, it’s static advice dressed up as something new.

What technologies power adaptive financial guidance?

Adaptive financial guidance is not a single tool. It’s a combination of several technologies and behavioral models working together.

Reinforcement learning is the engine at the center. Think of it as an agent that constantly observes your financial state, recommends an action (like increasing your emergency fund), and then measures whether that action moved you closer to your goal. Reinforcement learning continuously updates guidance based on user behavior feedback, which means the system gets more personalized the longer you use it. It’s not guessing. It’s learning.

Retrieval-Augmented Generation (RAG) is a method that pulls verified financial information into AI responses before they reach you. Combined with ethical filters, this approach produces significantly more accurate guidance. Systems using RAG and ethical filtering achieve 87.3% factual accuracy and reduce AI hallucinations from 34.2% to 9.1%. That matters because bad financial advice, even from an AI, has real consequences.

Near-real-time data is another key component. Many systems market themselves as “real-time,” but the practical standard is hourly or daily data refreshes. Near-real-time updates resolve the vast majority of data staleness complaints at a fraction of the cost of true streaming data. For personal finance decisions, that’s more than sufficient.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Behavioral finance principles round out the picture. These principles recognize that people make financial decisions based on emotion, habit, and cognitive shortcuts, not pure logic. Adaptive guidance systems use this knowledge to break large goals into smaller milestones, reduce the psychological weight of long-term planning, and keep you engaged when motivation dips.

“The most effective adaptive financial guidance systems don’t just crunch numbers. They account for how humans actually behave with money, building in checkpoints, encouragement, and course corrections that keep people on track through the inevitable ups and downs of real life.”

What are the practical benefits of adaptive financial guidance?

The benefits of adaptive financial guidance show up in three concrete areas: wealth accumulation, goal alignment, and reduced financial anxiety.

Better wealth outcomes over time

The 10% improvement in net wealth accumulation from adaptive systems is not a small number. On a $100,000 portfolio, that’s $10,000 more. On a $500,000 retirement account, it’s $50,000. The compounding effect over a 20 or 30-year horizon makes this difference substantial.

Staying on track through market volatility

Goal-aligned investing, a core feature of adaptive guidance, produces measurably better behavior during market downturns. Investors using goal-based frameworks stay invested during downturns far more consistently than those focused on benchmark comparisons. When your measure of success is “am I on track to buy a house in five years?” rather than “did I beat the S&P 500 this quarter?”, short-term volatility feels less threatening.

Reduced financial anxiety

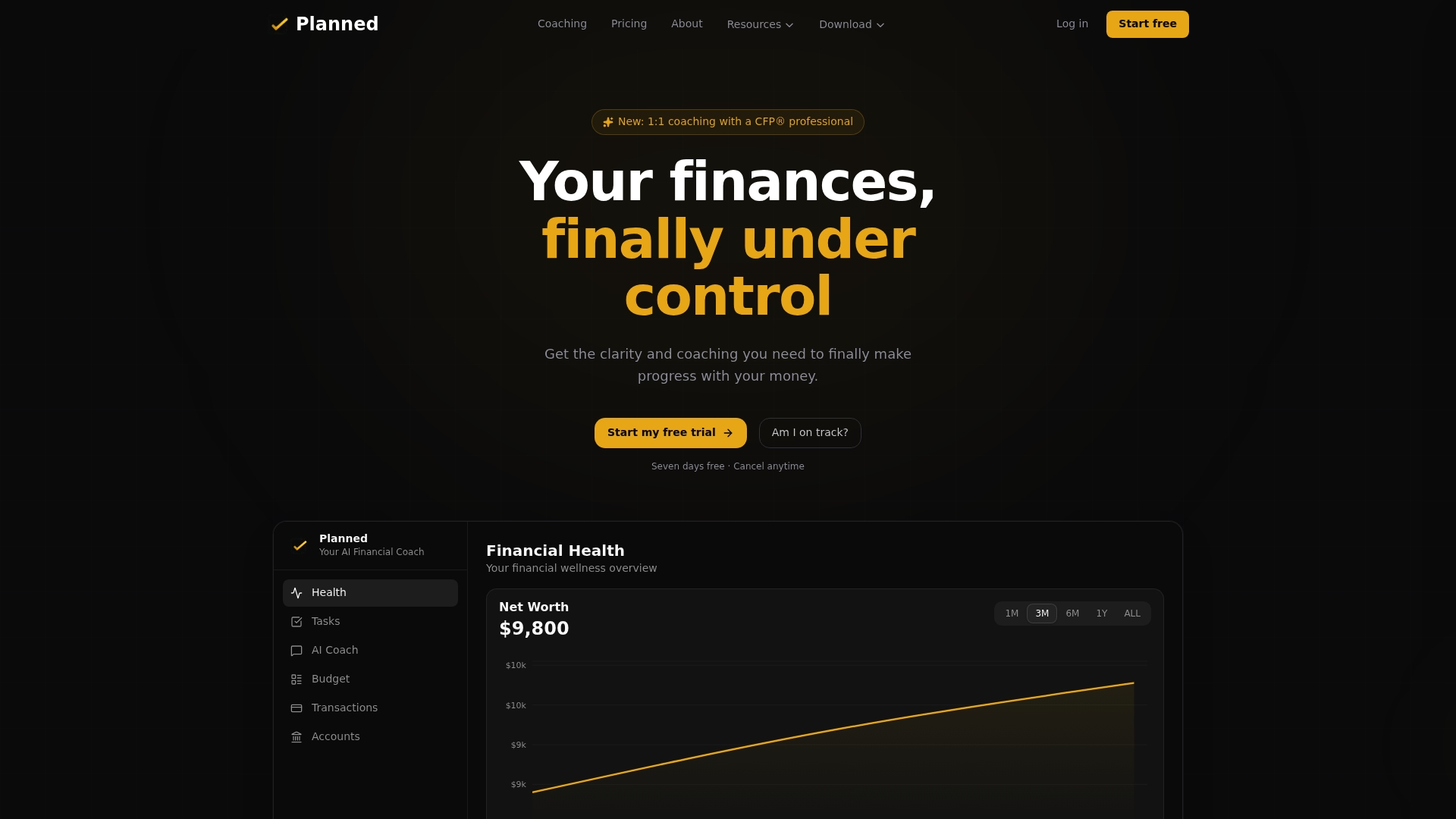

Breaking large goals into smaller, trackable milestones is one of the most effective ways to reduce financial anxiety. Behavioral finance reduces abandonment of long-term financial plans by making progress visible and achievable. Planned’s Financial Health Score does exactly this, giving you a clear number that reflects where you stand and what to focus on next.

Here’s a quick comparison of what adaptive guidance delivers versus the traditional model:

| Feature | Traditional advice | Adaptive guidance |

|---|---|---|

| Update frequency | Annual or semi-annual | Continuous (hourly/daily data) |

| Personalization | Based on a snapshot | Based on ongoing behavior |

| Goal tracking | Benchmark-focused | Life goal-focused |

| Response to life changes | Delayed | Near-immediate |

| Anxiety management | Limited | Built-in milestone coaching |

Pro Tip: Don’t wait for your annual review to adjust your financial plan. If you get a raise, change jobs, or take on new debt, update your goals immediately. Adaptive systems work best when your inputs are current.

How can you start using adaptive financial guidance today?

Getting started with adaptive financial guidance is more accessible than most people think. You don’t need a large portfolio or a high income. You need clear goals and the right tools.

-

Define your financial goals in specific terms. “Save more money” is not a goal. “Save $15,000 for a home down payment by december 2027” is. Adaptive systems need specific targets to measure progress and adjust recommendations.

-

Connect your real accounts. Adaptive guidance only works when the system can see your actual income, spending, and balances. Tools that rely on manually entered data miss the behavioral patterns that make personalization possible. Planned connects directly to your financial accounts for this reason.

-

Evaluate the technology behind any tool you use. Look for three things: explainability (can it tell you why it made a recommendation?), ethical safeguards (does it filter for accuracy?), and data refresh rates (how current is the information it uses?). These features separate genuine adaptive guidance from basic budgeting apps.

-

Combine AI guidance with human expertise when the stakes are high. AI excels at continuous monitoring and pattern recognition. A CFP® professional excels at nuanced judgment calls, like how to structure an inheritance or plan around a divorce. The best outcomes come from using both. Planned offers 1:1 coaching with CFP® professionals alongside its AI coach for exactly this reason.

-

Review your goals regularly, not just your numbers. Life changes your priorities. A goal that made sense at 25 may not fit at 32. Adaptive guidance works best when you treat your goals as living targets, not fixed destinations. Planned’s approach to adapting plans around life events reflects this philosophy directly.

-

Track behavioral patterns, not just balances. The real value of adaptive guidance is in what it reveals about your habits. Are you consistently overspending in one category? Is your savings rate drifting down? These patterns matter more than any single month’s balance.

Key Takeaways

Adaptive financial guidance outperforms static advice because it learns from your real behavior and adjusts continuously, producing measurably better financial outcomes over time.

| Point | Details |

|---|---|

| Core definition | Adaptive guidance updates recommendations continuously based on your actual behavior and goals. |

| Wealth advantage | Adaptive systems produce approximately 10% higher net wealth accumulation than static methods. |

| Technology foundation | Reinforcement learning, RAG, and ethical filters drive accuracy and personalization. |

| Goal alignment | Life goal-focused tracking keeps investors on course through market volatility better than benchmarks. |

| Anxiety reduction | Breaking goals into milestones reduces financial anxiety and prevents plan abandonment. |

Why I think most people are still getting financial advice backwards

Most financial advice is built around a product sale. You sit down with someone, they assess your situation, and within 30 minutes they’re recommending a specific fund, insurance policy, or account type. The advice is the wrapper. The product is the point.

Adaptive financial guidance flips that model. Behavioral coaching prioritized over product picking produces better long-term outcomes because it focuses on your behavior, not a transaction. The hardest part of personal finance is not picking the right ETF. It’s staying consistent when life gets complicated.

What I’ve seen over years of watching people manage money is that the biggest financial mistakes are behavioral, not analytical. People panic-sell during downturns. They abandon savings plans when an unexpected expense hits. They set goals in january and forget them by march. No static plan fixes those problems because static plans don’t respond to the moment when the behavior is happening.

The shift from annual to continuous financial planning is the most important structural change in personal finance right now. It’s not about technology for its own sake. It’s about having guidance that’s actually present when you need it, not waiting for you at your next scheduled appointment.

One caution: not everything marketed as “adaptive” or “AI-powered” actually qualifies. Ask whether the system learns from your specific data or just applies generic rules to your inputs. The difference matters enormously. Real adaptive guidance gets more accurate over time. Generic rule-based tools don’t.

Embrace the flexibility. Your financial life is not a straight line, and your guidance shouldn’t be either.

— Matt Schuberg

How Planned brings adaptive financial coaching to your goals

Planned is built on the principle that good financial guidance should know you, not just your account balances.

Planned connects an AI coach to your real financial accounts, giving you a personalized financial health score and specific guidance based on your actual income, spending, and goals. When your situation changes, your guidance changes with it. You can also use the savings priority calculator to figure out exactly where your next dollar should go, or book a session with a CFP® professional for guidance on bigger decisions. Early adopters report less financial anxiety and more confidence in their day-to-day money choices. That’s what adaptive guidance, done right, actually feels like.

FAQ

What is adaptive financial guidance in simple terms?

Adaptive financial guidance is personalized financial advice that updates automatically as your income, spending, and goals change. It uses AI and behavioral finance to keep your plan current without waiting for an annual review.

How does adaptive guidance differ from a standard budgeting app?

Standard budgeting apps track what you spend. Adaptive guidance systems analyze your behavior, learn from it, and recommend specific adjustments to help you reach your goals faster.

Is adaptive financial guidance the same as real-time financial guidance?

They are closely related but not identical. Most adaptive systems use near-real-time data (hourly or daily updates) rather than true real-time streaming. For personal finance decisions, near-real-time data provides sufficient accuracy and is more reliable.

Can adaptive financial guidance replace a human financial advisor?

Adaptive guidance excels at continuous monitoring and pattern recognition. Human advisors, especially CFP® professionals, add judgment on complex decisions. The strongest approach combines both, which is exactly how Planned is structured.

Does adaptive financial guidance recommend specific financial products?

No. Genuine adaptive guidance focuses on behavioral coaching, such as adjusting your savings rate or reallocating toward a goal, rather than recommending specific products. That distinction protects you from advice that serves a seller’s interest over your own.

Recommended

Ways to Benchmark Your Finances: A Practical Guide

Benchmark your finances with six metrics: emergency fund, debt-to-income, savings rate, housing, consumer debt, and investments. See where you stand today.

Financial Baseline Explained: Your Personal Finance Guide

A financial baseline is a fixed snapshot of your past income and spending. Here's how to set yours from 12 months of data and measure real progress each year.

10 Proven Ways to Reduce Financial Stress in 2026

Reduce financial stress in 2026 with 10 proven steps: a 20-minute budget, automated savings, a $500 emergency fund, and a debt payoff method that sticks.

Common Financial Advice Gaps to Fill in 2026

Financial advice gaps are blind spots in risk, taxes, estate, and investing that cost you money. Here's how to spot and fix the five biggest in 2026.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?