How to Optimize Finances Around Life Events

Learn how to optimize finances around life events. Make proactive adjustments to secure your future and manage life's milestones effectively.

How to Optimize Finances Around Life Events

TL;DR:

- Making proactive financial adjustments before and after major life events helps protect wealth and support future growth.

- Transition-based planning, focused on life changes as triggers, offers greater flexibility than traditional age-based methods.

Optimizing finances around life events means making targeted, proactive adjustments to your budget, savings, insurance, and investments before and after major personal milestones. Marriage, a new job, a baby, or a career change all shift your financial picture in ways that a static plan cannot handle. The good news is that each of these transitions is also an opportunity. With the right moves at the right time, you protect what you have built and set yourself up for what comes next.

What financial preparations should you make before a major life event?

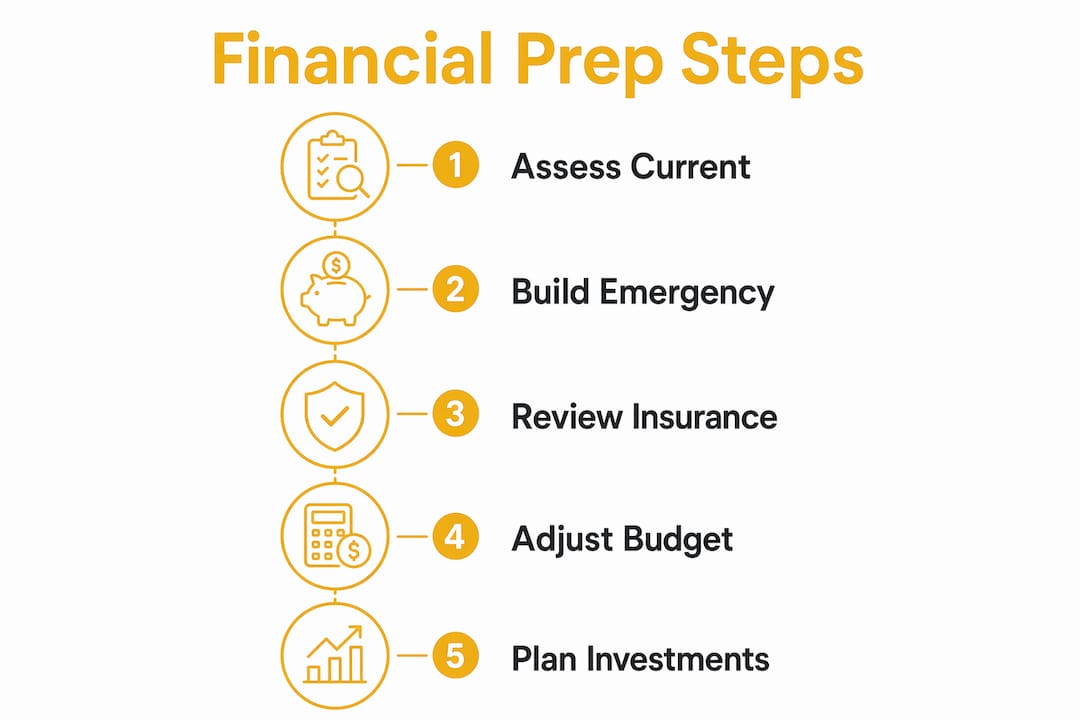

The best financial preparation starts with an honest look at where you stand today. Before any major change hits, run a quick financial health assessment to identify gaps. Think of it as taking a snapshot before the scenery changes.

Check your emergency fund first

Your emergency fund is the circuit breaker that keeps a life event from becoming a financial crisis. Standard guidance recommends 3–6 months of essential expenses saved in a liquid account. If your income is variable or you are the sole earner in your household, that target rises to 6–12 months. A job change or a new baby can disrupt cash flow for months, so having this buffer in place before the event matters more than having it afterward.

Review your budget benchmarks

A sound pre-event budget keeps essentials below 60% of your take-home pay and directs at least 20% toward savings and debt repayment. That 20% figure is not arbitrary. It reflects decades of financial planning research showing that households hitting this threshold consistently build wealth across life stages. If you are below it now, a life event is the perfect forcing function to close the gap.

Before the event, also review these key areas:

- Insurance coverage: Life, health, and disability policies often need updates after marriage, a new job, or a new dependent. Use a life insurance needs calculator to check whether your current coverage still fits.

- Tax implications: Marriage changes your filing status. A new job may shift your withholding. A side income or freelance work adds self-employment tax. Know what is coming before it arrives.

- Estate documents: A will, beneficiary designations, and a power of attorney are not just for retirees. Any major life change is a reason to create or update them.

Pro Tip: Start gathering financial documents, account statements, and insurance policies at least 60 days before a major event. Organization now prevents costly delays later.

| Preparation area | Action to take |

|---|---|

| Emergency fund | Build to 3–6 months of expenses (6–12 months for variable income) |

| Budget | Keep essentials below 60% of take-home pay |

| Insurance | Review and update life, health, and disability coverage |

| Taxes | Anticipate filing status or withholding changes |

| Estate documents | Update will, beneficiaries, and power of attorney |

How do you manage finances during and immediately after a life event?

The moment a life event happens, your financial priorities shift. Major life changes are financial turning points that require a proactive review of taxes, insurance, and spending. Waiting until things settle down is the most common and costly mistake people make.

Step-by-step financial actions for the transition period

- Reassess your cash flow. List your new income and new fixed expenses side by side. A new job may bring a higher salary but also higher commuting costs, new benefits premiums, or a gap between your last paycheck and your first new one.

- Rebuild or protect your emergency fund. If the event drew down your reserves, make replenishing them your first savings priority before resuming other goals.

- Update tax withholding. File a new W-4 with your employer after marriage, a new dependent, or a significant income change. Incorrect withholding leads to surprise tax bills or lost cash flow throughout the year.

- Coordinate financial roles. If you are merging finances with a partner, decide who manages which accounts, how joint expenses are split, and how each person’s savings goals are tracked.

- Consolidate where it makes sense. Simplifying finances during transitions by consolidating accounts and organizing documents reduces decision fatigue and makes your plan easier to manage.

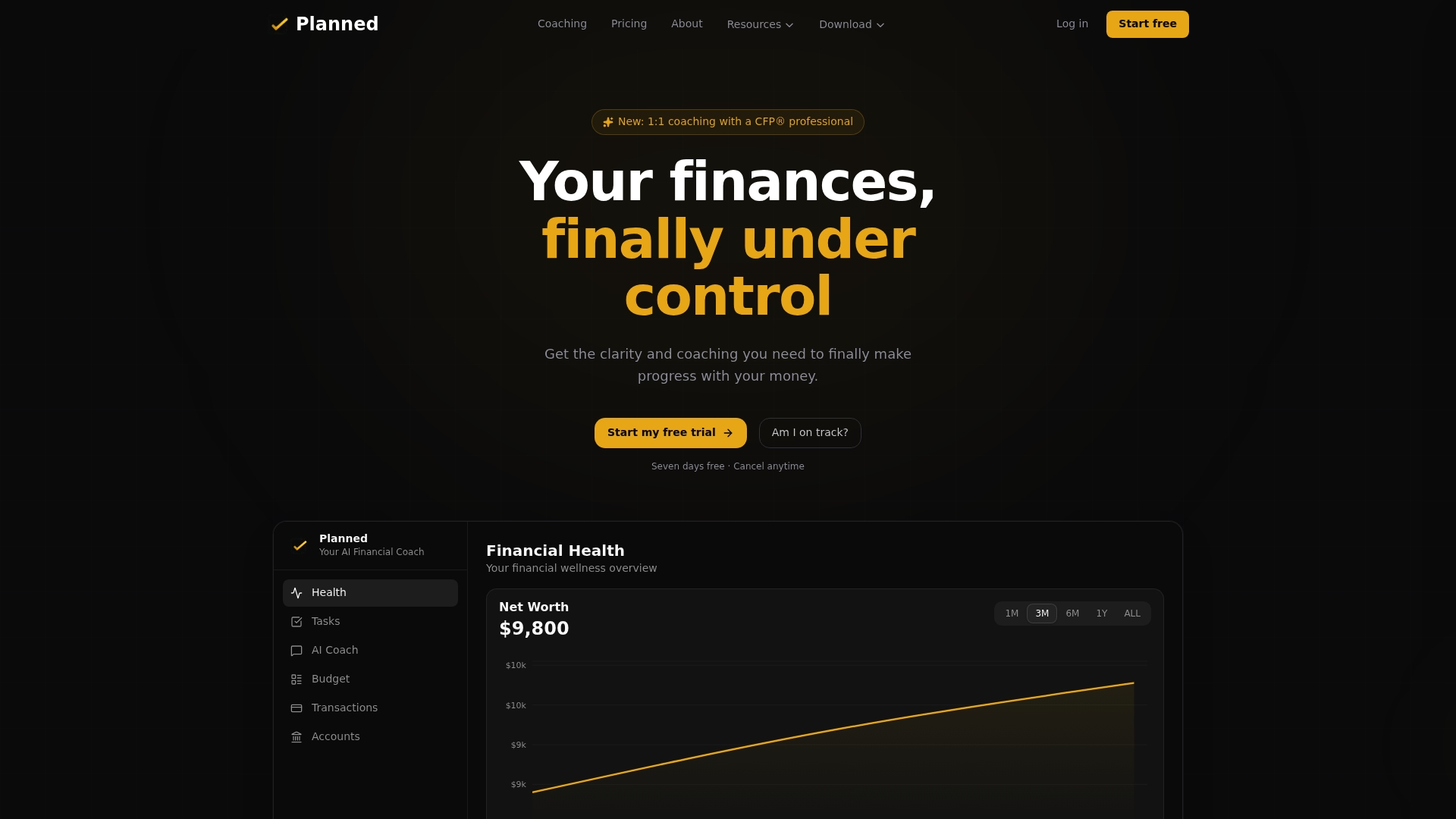

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Watch out for lifestyle creep

Lifestyle creep is the quiet budget killer that follows every raise or promotion. When income rises, spending tends to rise with it, often without a conscious decision. The fix is to automate your savings increase before you adjust your spending. If your new job pays $10,000 more per year, direct at least half of that increase to savings or investments before it hits your checking account.

Avoid these common post-event financial mistakes:

- Making large purchases before your new income is confirmed and stable

- Canceling insurance coverage during a job transition, even briefly

- Delaying beneficiary updates on retirement accounts and life insurance policies

- Treating a tax refund or signing bonus as regular income

Pro Tip: After any major life event, spend 30 minutes consolidating accounts and updating automatic transfers. Fewer accounts mean fewer things to track and fewer opportunities for money to slip through the cracks.

What long-term financial strategies help maintain stability after life changes?

Short-term adjustments get you through the transition. Long-term habits are what build lasting financial health. The key insight here is that transition-based planning accounts for unpredictable life events far better than planning around fixed age milestones. Life does not follow a schedule. Your financial plan should not either.

Build toward retirement savings milestones

Age-based benchmarks give you a useful reference point. Standard guidance suggests having 1x your annual salary saved by age 30 and 2x by age 35. Use Planned’s net worth calculator to see where you stand against these targets and identify the gap you need to close.

Redirect raises before lifestyle catches up

Lifestyle inflation during career advancement is one of the biggest threats to long-term financial goals. Every raise feels like breathing room. But if spending rises in lockstep with income, your savings rate stays flat no matter how much you earn. Planned’s raise and lifestyle creep allocator helps you decide exactly how much of a raise to keep and how much to redirect toward investments. The article Why Your Raises Aren’t Making You Richer breaks down why this pattern is so common and how to break it.

Build consistency over perfection

Consistency in saving and investing over decades matters more than timing the market or finding the perfect allocation. A person who saves steadily through job changes, a wedding, and a new baby will outperform someone who pauses contributions during each transition. Automate contributions so they happen regardless of what else is going on in your life.

Here is how a long-term financial maintenance plan compares across two approaches:

| Approach | Focus | Strength | Weakness |

|---|---|---|---|

| Stage-based planning | Fixed age milestones | Predictable benchmarks | Fails when life does not follow the schedule |

| Transition-based planning | Life events as triggers | Flexible and resilient | Requires regular reassessment |

Pro Tip: Schedule a 30-minute financial review every six months, not just when something changes. Treat it like a calendar appointment. Successful individuals treat financial management as an ongoing conversation, not a one-time fix.

Which tools and resources help with financial management during transitions?

The right tools make financial planning for life changes far less daunting. They give you a clear picture of where you stand and what to do next, without requiring a finance degree to use.

Planned offers a suite of free financial tools built specifically for moments like these:

- Savings Priority Calculator: Tells you which savings goals to fund first based on your actual situation. Useful when cash flow is tight and you need to make trade-offs.

- Life Insurance Needs Calculator: Calculates how much coverage you actually need after a major life change, rather than relying on a generic rule of thumb.

- Net Worth Calculator with Age Benchmarks: Shows your current net worth against age-based targets so you know whether you are ahead, on track, or behind.

- Raise and Lifestyle Creep Allocator: Helps you split a raise between lifestyle improvements and long-term savings in a way that serves both goals.

Beyond tools, working with a financial advisor or coach during a major transition adds a layer of accountability and personalization that no calculator can fully replace. A coach who can see your actual accounts, income, and spending patterns gives you guidance that fits your life, not a generic template. Planned’s AI coach connects directly to your financial accounts and delivers personalized guidance based on your real numbers, including a Financial Health Score that shows you exactly where you stand.

For self-directed planning, the 10 pillars of a comprehensive financial plan is a strong starting framework. It covers everything from cash flow management to estate planning in a format you can work through at your own pace.

Key Takeaways

Effective budgeting for life milestones requires proactive preparation before the event, disciplined adjustments during the transition, and consistent long-term habits that protect your financial health regardless of what life throws at you.

| Point | Details |

|---|---|

| Prepare before the event | Build your emergency fund and review insurance before the life change arrives. |

| Adjust cash flow immediately | Reassess income and expenses right away and update tax withholding after any major change. |

| Avoid lifestyle creep | Redirect raises to savings before spending adjusts upward to match new income. |

| Use transition-based planning | Plan around life events as triggers, not fixed age milestones, for greater resilience. |

| Stay consistent over time | Steady saving through every transition outperforms pausing contributions to time things perfectly. |

Why I think most financial advice misses the point on life transitions

Most financial advice treats life events as interruptions to an otherwise orderly plan. Get married, update your beneficiaries, done. Have a baby, open a 529, done. That checklist mentality is better than nothing, but it misses what actually makes or breaks financial outcomes during transitions.

The real challenge is emotional. When life changes fast, financial decisions get made from anxiety, not analysis. I have seen people cash out retirement accounts during job losses because the balance felt abstract and the fear felt real. I have seen couples avoid money conversations entirely after merging finances because the conflict felt too uncomfortable. These are not knowledge failures. They are emotional ones.

The most effective approach I have seen is treating each major life event as a reason to build an entirely new financial plan, not patch the old one. Using life events as catalysts to build new plans, rather than fitting old budgets to new realities, produces far better outcomes. That reframe changes everything. Instead of asking “how do I adjust my budget for this wedding?” you ask “what does my financial life need to look like after this wedding?” The second question leads to a much better answer.

The other thing worth saying plainly: simplicity wins. Every account you consolidate, every automatic transfer you set up, every document you organize is one less thing that can go wrong during a stressful period. Financial complexity is not sophistication. It is friction. Reduce it wherever you can.

— Matt Schuberg

How Planned supports your financial planning during life changes

Life transitions are exactly when personalized financial guidance matters most. Generic advice cannot account for your specific income, debt load, or savings rate. Planned connects you to an AI coach that reads your actual financial accounts and gives you guidance built around your real numbers, including a Financial Health Score that tells you where you stand at a glance.

For those who want a human in their corner, Planned offers 1:1 coaching with a CFP® professional who can walk you through every financial decision a major life event triggers. Whether you are preparing for a wedding, starting a new job, or planning for a growing family, a dedicated coach helps you move with confidence instead of guesswork. You can also access Planned’s full suite of free planning tools to start building clarity on your own terms.

FAQ

What does it mean to optimize finances around life events?

It means making proactive, targeted adjustments to your budget, savings, insurance, and investments before and after major personal milestones. The goal is to protect existing wealth and position yourself for growth through the transition.

How much should I have saved before a major life event?

Standard guidance recommends an emergency fund of 3–6 months of essential expenses before any major transition. Single-income households or those in volatile industries should target 6–12 months to account for higher income risk.

What is the biggest financial mistake people make during life transitions?

The most common mistake is delaying financial updates, such as beneficiary changes, insurance reviews, and tax withholding adjustments, until after the dust settles. These delays create real costs and coverage gaps that are difficult to reverse.

How is transition-based planning different from traditional financial planning?

Transition-based planning treats life events as the triggers for financial reassessment rather than relying on fixed age milestones. This approach is more flexible and better suited to the unpredictable way real life actually unfolds.

How can I prevent lifestyle creep after a raise or promotion?

Automate a savings increase before your new income reaches your checking account. Directing at least half of any raise toward investments or savings before adjusting spending keeps your savings rate growing alongside your income.

Recommended

Types of Personalized Financial Guidance: 2026 Guide

Personalized financial guidance includes credit counseling, CFP® professionals, coaching, and AI tools. Here's how to pick the right one for your money goals.

The Role of Financial Habits in Saving: Your Guide

Financial habits drive consistent saving by replacing willpower with automation. Build routines that make saving the default, even when money is tight.

How to Interpret Your Personal Finance Dashboard

A personal finance dashboard shows net worth, cash flow, and budget variances. Here's how to read each metric and turn the numbers into real decisions.

Financial Health Assessment Best Practices That Work

A financial health assessment follows a simple cycle: assess, plan, execute, reassess. Here are the best practices that actually move your money forward.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?