How to Personalize Your Financial Plan by Income

Learn how to personalize financial plan your income for real results. Transform your earnings into a tailored strategy that works for you.

How to Personalize Your Financial Plan by Income

TL;DR:

- A personalized financial plan is built around your actual income, expenses, and goals, not a generic template. Knowing your true total income and tracking actual spending helps create a reliable plan that adapts over time. Regular updates and appropriate insurance coverage safeguard your financial future as your circumstances change.

A personalized financial plan is a living strategy built around your specific income, expenses, and goals rather than a generic template. Most standard financial advice assumes a steady salary, average expenses, and a one-size-fits-all savings rate. Your income is not average. It is yours. Knowing how to personalize a financial plan around your income is the difference between a plan that sits in a drawer and one that actually moves you forward. The industry term for this process is personal financial planning, and when done right, it produces measurably better outcomes than any off-the-shelf approach.

How to personalize a financial plan around your income

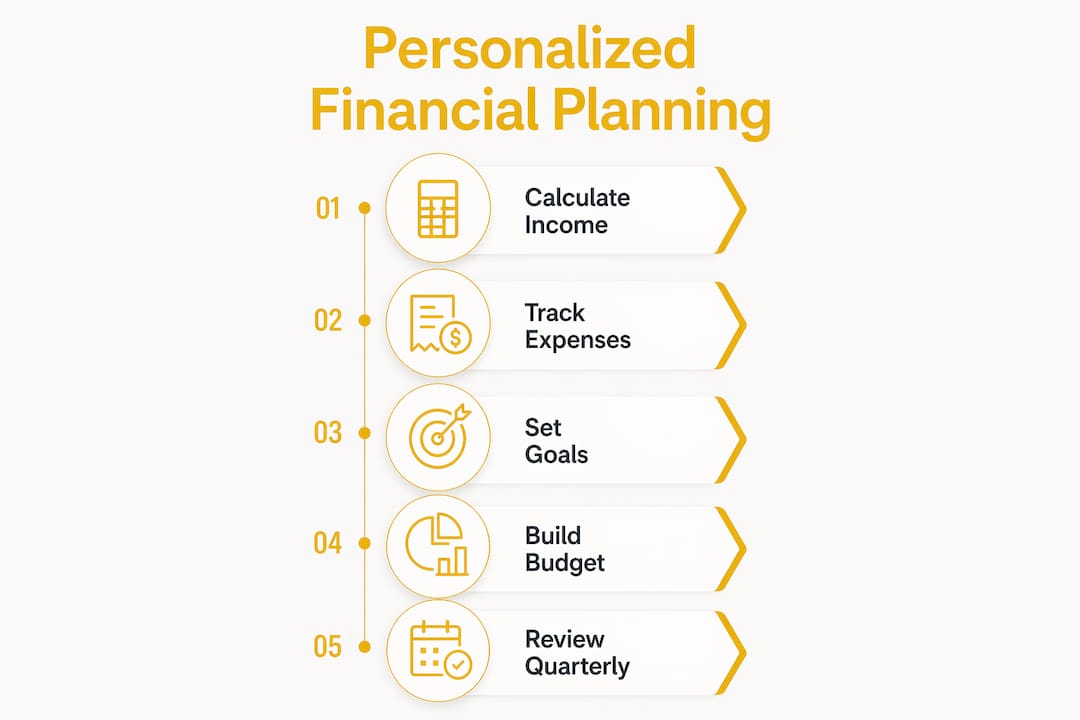

The first step is knowing exactly what you earn. That sounds obvious, but most people undercount their total income by forgetting side gigs, freelance payments, bonuses, or rental income. Add every source together to get your true gross income, then calculate your net income after taxes and deductions. That net number is your real starting point.

From there, map your monthly expenses into three buckets using the 50/30/20 rule: 50% for needs like rent and groceries, 30% for wants like dining out and subscriptions, and 20% for savings and debt repayment. This benchmark is not a rigid law. It is a diagnostic tool. If your needs eat 65% of your income, the rule tells you exactly where the pressure is coming from.

Pro Tip: Track three months of actual spending before you build any plan. Most people overestimate their savings rate by 8–12 percentage points when they rely on memory alone.

Here are the essential data inputs you need before building your plan:

| Data Input | Why It Matters |

|---|---|

| Gross and net monthly income | Sets the ceiling for every budget category |

| Fixed monthly expenses | Identifies non-negotiable obligations |

| Variable monthly expenses | Reveals where spending flexibility exists |

| Total debt balances and interest rates | Determines payoff priority and cost |

| Current savings and investment balances | Shows your starting point for growth |

| Income volatility range | Protects the plan during low-earning months |

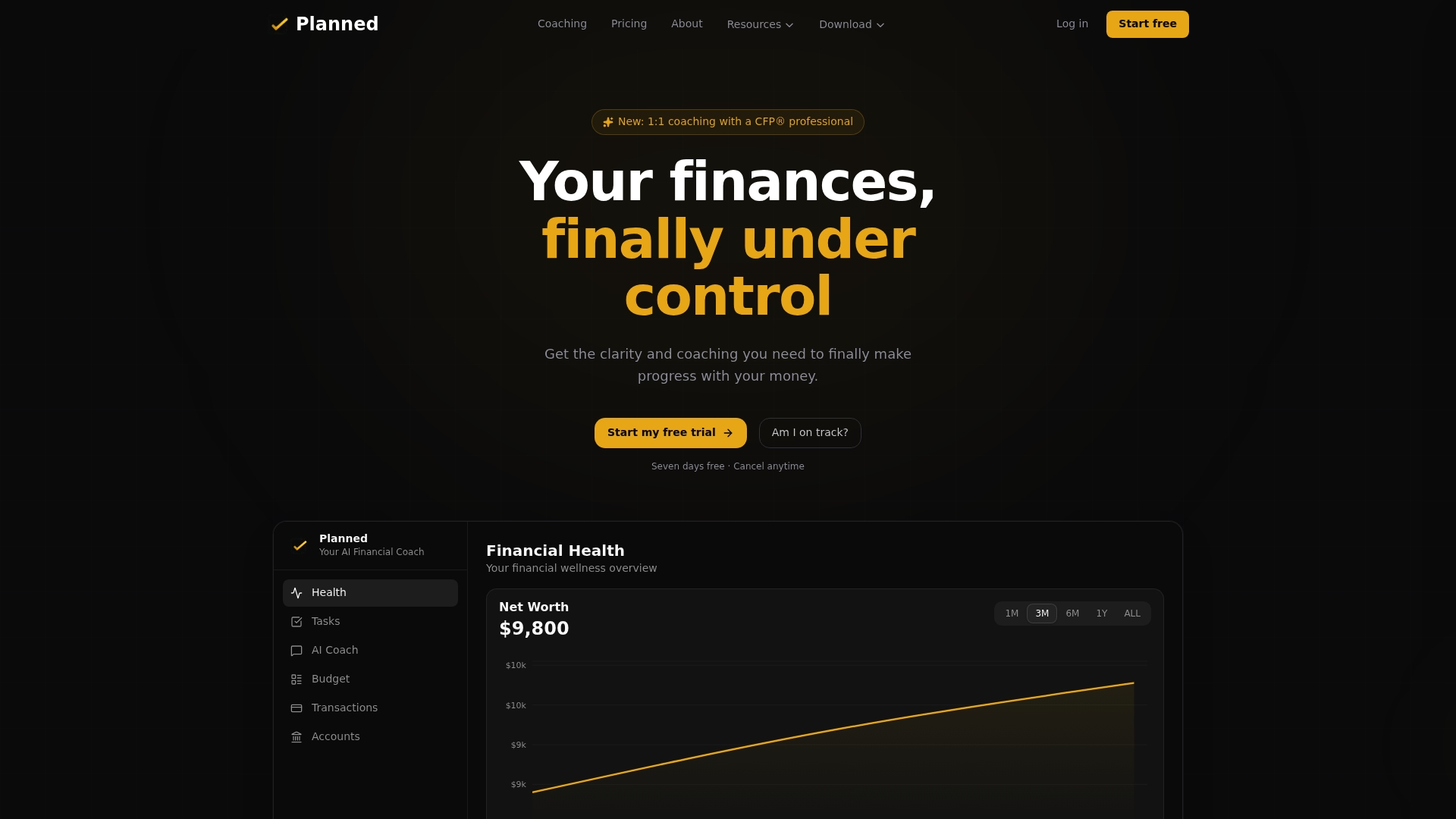

AI-driven financial planning apps can automate this data gathering and flag gaps you might miss manually. Planned, for example, connects directly to your real financial accounts and surfaces patterns in your spending that are invisible in a spreadsheet.

If your income is irregular, model it over 6–12 months and build your plan around your lowest monthly figure, not your average. That single adjustment makes a plan resilient instead of fragile.

What saving and investing strategies match your income level?

Saving rates are not one-size-fits-all. Financial experts recommend a total savings rate of 20–25% of gross income, with 15–20% dedicated specifically to retirement. If you are early in your career or carrying high-interest debt, starting at 10% is a realistic and sustainable entry point. The goal is to build the habit first, then increase the rate as income grows.

Which accounts you prioritize depends heavily on your income bracket. The order matters because each account type carries different tax advantages.

- Emergency fund first. Three to six months of expenses in a high-yield savings account before anything else. This is the circuit breaker that keeps one bad month from derailing your entire plan.

- Employer 401(k) match. Capture every dollar of employer match before contributing elsewhere. An unmatched contribution is a 50–100% guaranteed return you are leaving on the table.

- High-interest debt. Any debt above 7% interest should be paid down aggressively before investing beyond the employer match.

- Roth IRA or traditional IRA. Mid-income earners benefit most from Roth contributions while their tax rate is still relatively low.

- Health Savings Account (HSA). Mid-income earners with high-deductible health plans gain triple tax advantages through HSAs: contributions are pre-tax, growth is tax-free, and qualified withdrawals are tax-free.

- Taxable brokerage accounts. Once tax-advantaged accounts are maxed, a taxable account gives you flexibility without withdrawal restrictions.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

For higher earners, the picture shifts. High-income professionals earning $250,000 or more face marginal tax rates exceeding 47%, which means budgeting alone is not enough. Tax-efficient structures like backdoor Roth IRA conversions, mega backdoor Roth contributions through after-tax 401(k) plans, and donor-advised funds become the real levers for wealth building. Investment priorities shift toward alternative investments and tax-loss harvesting strategies at this income level.

Pro Tip: Always capture your full employer 401(k) match before directing money anywhere else. It is the only guaranteed return in personal finance.

How do you build a financial roadmap that adapts over time?

A financial plan is not a document you write once and file away. Successful personalized planning treats the plan as a living document that updates as your income and life circumstances change. That mindset shift is what separates people who reach their goals from those who feel perpetually behind.

Set goals across three time horizons. Short-term goals cover the next 12 months: building your emergency fund, paying off a credit card, or saving for a specific purchase. Mid-term goals span one to five years: a home down payment, a career transition fund, or starting a business. Long-term goals extend beyond five years and center on retirement, financial independence, or generational wealth.

Retirement income planning should move beyond simple rules of thumb. Month-by-month income modeling that accounts for Social Security timing, pension income, and investment withdrawals produces far more accurate projections than the 4% rule alone. Your income in retirement is as personal as your income today.

Life events require plan updates. Review your financial roadmap when any of these occur:

- A job change or significant salary increase or decrease

- Marriage, divorce, or a new dependent

- Buying or selling a home

- Receiving an inheritance or windfall

- A health event that affects income or expenses

Pro Tip: Schedule a 30-minute plan review every quarter. Set a recurring calendar reminder and treat it like a bill payment. Consistency beats intensity every time.

Planned’s financial tools for life events walk you through exactly how to recalibrate your numbers after a major change without starting from scratch.

Why does insurance belong in your income-based financial plan?

Insurance is the part of financial planning that most people ignore until something goes wrong. Improperly aligned insurance coverage leaves high earners especially vulnerable, because their lifestyle, liabilities, and income replacement needs are significantly larger than a standard policy covers.

The core insurance types every income-based plan should address are:

- Life insurance. Coverage should replace 10–12 times your annual income to protect dependents from financial disruption.

- Disability insurance. Your income is your most valuable asset. Long-term disability coverage protects it if illness or injury prevents you from working.

- Health insurance. Pair your plan with an HSA if you qualify. The tax savings compound meaningfully over time.

- Property and liability insurance. As your net worth grows, umbrella liability coverage protects assets that standard homeowner or renter policies do not.

The right coverage amount is not a guess. It is a calculation based on your income, your debts, your dependents, and your existing assets. A $60,000 earner and a $200,000 earner have fundamentally different exposure. Treating them the same way is how coverage gaps happen.

Pro Tip: Review your insurance coverage every time your income increases by 20% or more. Most people set it and forget it, then discover the gap at the worst possible moment.

Personalized financial guidance that accounts for insurance as part of the income picture gives you a complete view of your financial health, not just your savings balance.

Key Takeaways

A personalized financial plan built around your actual income, not a generic template, is the most reliable path to financial confidence and long-term wealth.

| Point | Details |

|---|---|

| Start with real income data | Calculate total net income including all sources before setting any budget or savings target. |

| Use the 50/30/20 rule as a diagnostic | Apply the benchmark to reveal where income pressure exists, then adjust categories to fit your reality. |

| Match savings strategy to income bracket | Prioritize accounts in order: emergency fund, employer match, debt, IRA, HSA, then taxable accounts. |

| Treat the plan as a living document | Review and update your roadmap quarterly and after every major life or income change. |

| Align insurance to your actual income | Calculate coverage based on income, debts, and dependents rather than defaulting to minimum policy limits. |

Why I think most financial plans fail before they start

The most common mistake I see is people building a financial plan around the income they hope to have rather than the income they actually have. It feels motivating in the moment. In practice, it produces a plan that falls apart the first time reality shows up.

One-size-fits-all strategies fail because they ignore the mathematical reality of different income levels and life phases. A 25-year-old earning $48,000 and a 42-year-old earning $180,000 need fundamentally different strategies, not the same blog post with different numbers plugged in. The accounts they should prioritize, the tax moves available to them, and the insurance they need are all different.

The other thing I have noticed is that people treat a financial plan like a report card rather than a navigation tool. They feel bad when they miss a savings target and abandon the whole thing. A plan that adapts to a bad month is not a failure. It is doing exactly what a good plan should do.

Technology has genuinely changed what is possible here. Connecting your plan to real account data, the way Planned does, means your numbers are always current. You are not working from a snapshot you took six months ago. That real-time connection is what makes a plan feel manageable instead of like a chore.

The best financial plan is not the most sophisticated one. It is the one you actually follow, update, and trust. Build it around your real income, review it regularly, and give yourself permission to adjust it as your life changes.

— Matt Schuberg

Planned makes your income-tailored financial plan real

Building a financial plan that actually fits your income takes more than a spreadsheet. Planned connects your real financial accounts to an AI coach that gives you answers based on your actual numbers, not generic benchmarks.

Whether you are mapping out a savings priority strategy for the first time or recalibrating after a major income change, Planned gives you the tools and the guidance to move forward with confidence. The Financial Health Score shows you exactly where you stand today. One-on-one coaching with a CFP® professional gives you a real expert to work through the decisions that matter most. Your income is specific to you. Your financial plan should be too. Get started with Planned and build a roadmap that actually reflects your life.

FAQ

What does it mean to personalize a financial plan by income?

Personalizing a financial plan by income means building your budget, savings rate, investment priorities, and insurance coverage around your specific earnings rather than generic benchmarks. The 50/30/20 rule and savings rate targets of 20–25% are starting points, not fixed rules.

How much should I save based on my income?

Financial experts recommend saving 20–25% of gross income overall, with 15–20% directed toward retirement. Starting at 10% is sustainable if you are early in your career or paying down high-interest debt.

What accounts should I prioritize at different income levels?

Lower and mid-income earners should prioritize emergency funds, employer 401(k) matches, and Roth IRAs. Higher earners benefit from maxing HSAs, using backdoor Roth IRA strategies, and directing funds into donor-advised funds or taxable brokerage accounts.

How often should I update my financial plan?

Review your plan every quarter and after any major life event such as a job change, marriage, or home purchase. A personalized plan is a living document, not a one-time exercise.

How do I handle irregular income in a financial plan?

Average your income over 6–12 months and build your plan around your lowest monthly figure. That approach protects your commitments during slow months without requiring you to cut back every time income dips.

Recommended

What Is Financial Mental Load and How to Manage It

Financial mental load is the ongoing background effort of managing your money. Learn what it is, who carries it most, and practical ways to reduce it.

Why Financial Goals Need Tracking to Actually Work

Tracking financial goals is what turns intention into real results. See which metrics matter, how often to review, and how to build a habit that sticks.

The Financial Planning Process: A Step-by-Step Guide

The financial planning process is a seven-step cycle to set goals, budget, save, and pay off debt. Here's how each step works and where to begin today.

How to Optimize Finances Around Life Events

Optimizing finances around life events means adjusting your budget, savings, and insurance before and after milestones like marriage, a new job, or a baby.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?