What Does Financial Profile Mean? Your 2026 Guide

Discover what a financial profile means and how it shapes your financial health. Learn to make smarter money decisions today!

What Does Financial Profile Mean? Your 2026 Guide

TL;DR:

- A financial profile summarizes your income, expenses, assets, and liabilities at a specific time. It helps you understand your current financial health and improves your borrowing prospects. Regularly updating your profile allows for better personal planning and credit evaluation.

A financial profile is a snapshot of your complete financial condition at a specific point in time, covering your income, expenses, assets, and liabilities. Think of it as your financial report card. It tells you, your lender, or your financial advisor exactly where you stand right now. Understanding your financial profile gives you the foundation to make smarter decisions about borrowing, saving, and planning for the future.

What does financial profile mean, and what does it include?

A financial profile is defined as a structured summary of your financial condition, capturing four core elements: income, expenses, assets, and liabilities. These four components work together to reveal your net worth, your cash flow, and your overall financial health. Creating a financial profile involves five key steps: gathering data, analyzing cash flow, assessing net worth, identifying goals, and developing a strategy. That process turns raw numbers into a picture you can actually use.

The term “financial profile” is the everyday phrase most people search for. The formal industry equivalent is a Statement of Financial Position, which you will encounter in accounting and lending contexts. Both terms describe the same core concept: a structured view of what you own, what you owe, and what flows in and out.

Pro Tip: Start your financial profile by listing every account you hold, including checking, savings, retirement, and any loans. That list alone reveals more than most people expect.

The four core components explained

| Component | What it includes | Why it matters |

|---|---|---|

| Income | Salary, freelance earnings, rental income, dividends | Drives your ability to cover expenses and save |

| Expenses | Rent, utilities, groceries, subscriptions, debt payments | Determines your monthly cash flow |

| Assets | Cash, investments, property, vehicles, retirement accounts | Builds net worth over time |

| Liabilities | Mortgages, student loans, credit card balances, car loans | Reduces net worth and affects borrowing power |

Your net worth is simply assets minus liabilities. A positive net worth means you own more than you owe. That single number is one of the most telling indicators of financial health. You can calculate yours right now with a net worth calculator that also shows how you compare to age benchmarks.

Why is a strong financial profile important?

A strong financial profile directly determines your borrowing power, your access to credit, and your ability to reach long-term goals. Lenders prioritize borrowers with low debt-to-income ratios and high credit scores as definitive indicators of disciplined financial management. That means two people with identical incomes can receive very different loan offers based on how their profiles look.

Your debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments. Lenders use it as a quick filter. A DTI above 43% typically disqualifies you from most conventional mortgages. Keeping it below 36% puts you in a strong position.

Beyond the numbers, lenders factor in lifestyle habits such as bill payment patterns and discretionary spending ratios, which can override simple income metrics. That means even with a solid salary, erratic spending or late payments can weaken your profile significantly. Consistency matters as much as the dollar amounts.

Here is what lenders typically evaluate when reviewing your financial profile:

- Credit score: A FICO score above 700 signals reliability.

- Debt-to-income ratio: Lower is better; below 36% is the target.

- Payment history: Late payments stay on your credit report for seven years.

- Asset reserves: Savings and investments show you can weather financial setbacks.

- Employment stability: Consistent income reduces perceived lending risk.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Pro Tip: Improving your financial profile does not require a dramatic overhaul. Small consistent improvements in financial habits, like paying bills on time and reducing one recurring expense, can meaningfully increase your borrowing potential over six to twelve months.

How does a financial profile differ between personal and business use?

Personal financial profiles and business financial profiles share the same logic but serve different purposes and follow different standards. Your personal profile focuses on individual income, personal debts, and household expenses. A business financial profile, by contrast, follows the formal accounting equation: Assets = Liabilities + Equity. This is the basis of the Statement of Financial Position, the document analysts use to assess a company’s financial health.

| Dimension | Personal financial profile | Business financial profile |

|---|---|---|

| Primary document | Personal balance sheet | Statement of Financial Position |

| Key metrics | Net worth, DTI, credit score | Liquidity, solvency, profitability |

| Time frame | Current snapshot | Multi-year comparative data |

| Audience | Individual, lenders, advisors | Investors, regulators, creditors |

| Governing standard | Credit bureau guidelines | GAAP or IFRS accounting standards |

For businesses, comparative financial data over a three-year period is ideal for accurately gauging financial health markers such as liquidity, profitability, and solvency. That multi-year view reveals trends that a single snapshot cannot. A company might look healthy in one year but show a declining pattern when you zoom out.

For individuals, the same principle applies. A strong financial position features minimal debt and large cash and investment reserves, shaped by profitability and asset management over time, not just a single month’s numbers. Your profile today is a starting point, not a final verdict.

How to create and maintain your financial profile

Building your financial profile is a five-step process. Each step builds on the last, so accuracy at the start matters.

- Gather your data. Collect statements for every bank account, investment account, loan, and credit card. Include your most recent pay stubs and any other income sources.

- Analyze your cash flow. Subtract your total monthly expenses from your total monthly income. A positive number means you are building wealth. A negative number means you are spending more than you earn.

- Assess your net worth. Add up all your assets. Subtract all your liabilities. The result is your net worth. Review financial health best practices to understand what your number means in context.

- Identify your goals. Are you saving for a home, paying off debt, or building an emergency fund? Your goals shape which parts of your profile need the most attention.

- Develop a strategy. Use your cash flow and net worth data to set a realistic plan. Prioritize high-interest debt, build savings, and track progress monthly.

Maintaining your profile is just as important as building it. Errors in reported debt or bank account data may cause loan denials during credit checks. That means one outdated account balance or an incorrectly reported debt can trigger an automated rejection before a human ever reviews your application.

Best practices for keeping your profile accurate and current:

- Review your credit report at least once a year and dispute any errors promptly.

- Update your asset and liability list every quarter, or whenever a major financial event occurs.

- Track your spending monthly so your expense data stays current.

- Monitor your financial habits and adjust when patterns shift.

- Keep records of income changes, especially if you are self-employed or have variable pay.

Pro Tip: Set a recurring calendar reminder every quarter to update your net worth. Seeing it move in the right direction, even by a small amount, builds the motivation to keep going.

Key Takeaways

A financial profile is the single most useful document for understanding where you stand financially and what steps will move you forward.

| Point | Details |

|---|---|

| Core definition | A financial profile captures income, expenses, assets, and liabilities at a specific point in time. |

| Net worth is central | Subtract total liabilities from total assets to get the number that defines your financial position. |

| Lenders look beyond income | Debt-to-income ratio, credit score, and lifestyle habits all shape how lenders read your profile. |

| Accuracy prevents denials | A single data error in your profile can trigger an automated loan rejection during a credit check. |

| Profiles require regular updates | Reviewing and updating your profile quarterly keeps it reliable for both personal planning and external evaluations. |

Financial profiles are living documents, not report cards

Most people treat their financial profile like a test score: something to check once, feel good or bad about, and move on. That is the wrong approach. A financial profile is a living document. It changes every time your income shifts, a debt gets paid off, or your investment account grows. The real insight comes from watching it change over time.

I have seen people with impressive salaries carry profiles that would concern any lender, because their spending patterns and debt load told a different story than their income alone. I have also seen people with modest incomes carry profiles that opened every financial door they wanted, because they had spent years keeping their DTI low and their savings consistent. The number on your paycheck is just one input.

The most common mistake I see is treating the financial profile as a one-time exercise. Someone builds it before applying for a mortgage, gets the loan, and never looks at it again. Then two years later, they want to refinance or take out a business loan, and they are starting from scratch with outdated data. The people who benefit most from their financial profiles are the ones who treat them the way athletes treat game film: reviewing them regularly, looking for patterns, and making small corrections before problems compound.

Your financial profile does not need to be perfect to be useful. It needs to be honest and current. Even a profile that shows more debt than you would like gives you a clear target. You can learn how to read your financial health report and turn those numbers into a plan that actually moves the needle.

— Matt Schuberg

Your financial profile, made clear with Planned

Understanding your financial profile is one thing. Knowing what to do with it is another.

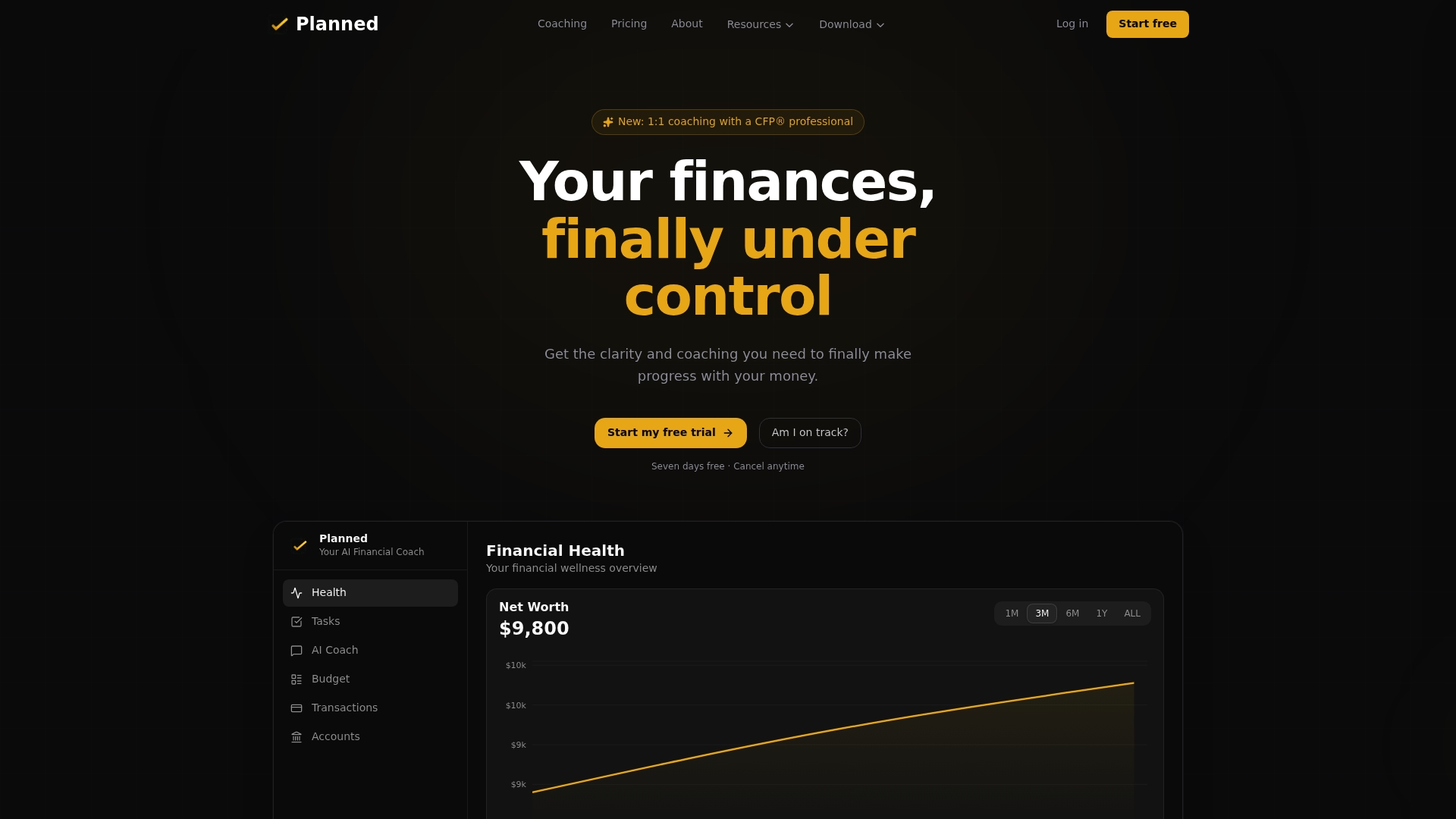

Planned connects directly to your real financial accounts and gives you a Financial Health Score based on your actual numbers, not generic benchmarks. You can ask specific questions about your income, spending, and debt, and get answers tailored to your situation. Whether you want to improve your borrowing power, track your net worth, or build a plan around your goals, 1:1 financial coaching with a CFP® professional through Planned gives you a real person in your corner. You can also explore free financial tools to start building your profile today.

FAQ

What does financial profile mean in simple terms?

A financial profile is a summary of your income, expenses, assets, and liabilities at a specific point in time. It shows your net worth and cash flow, giving you and any lender a clear picture of your financial condition.

What is the most important number in a financial profile?

Net worth is the single most telling number. It is calculated by subtracting your total liabilities from your total assets, and it reflects your overall financial position more accurately than income alone.

How does a financial profile affect loan approval?

Lenders use your financial profile to evaluate your debt-to-income ratio, credit score, and payment history. A profile with low debt, consistent payments, and healthy reserves significantly increases your chances of approval and better loan terms.

How often should you update your financial profile?

Updating your financial profile at least once per quarter keeps the data accurate and useful. Errors in reported debt or account balances can trigger automated loan rejections, so current information protects you during credit evaluations.

What is the difference between a personal and a business financial profile?

A personal financial profile focuses on individual net worth, income, and debts. A business financial profile follows the formal Statement of Financial Position and tracks liquidity, solvency, and profitability, often across multiple years to identify performance trends.

Recommended

How to Personalize Your Financial Plan by Income

Personalize your financial plan by income: total your real earnings, match your savings rate to your bracket, and review it quarterly as life changes.

What Is Financial Mental Load and How to Manage It

Financial mental load is the ongoing background effort of managing your money. Learn what it is, who carries it most, and practical ways to reduce it.

Why Financial Goals Need Tracking to Actually Work

Tracking financial goals is what turns intention into real results. See which metrics matter, how often to review, and how to build a habit that sticks.

The Financial Planning Process: A Step-by-Step Guide

The financial planning process is a seven-step cycle to set goals, budget, save, and pay off debt. Here's how each step works and where to begin today.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?