Financial Anxiety Management Best Practices That Work

Discover effective financial anxiety management best practices. Learn budgeting tips and psychological techniques to reduce money stress.

Financial Anxiety Management Best Practices That Work

TL;DR:

- Managing financial anxiety involves combining realistic budgeting with psychological techniques like CBT to address both money and emotional stress. Building a small emergency fund and scheduling regular financial reviews can significantly reduce anxiety over time. Professional support from coaching or therapy helps target emotional roots and sustain long-term wellness.

Financial anxiety management best practices combine structured financial planning with proven psychological techniques to reduce money stress and improve decision-making. The clinical term for this integrated approach is financial stress management, and it draws from both behavioral finance and cognitive-behavioral therapy (CBT). Fidelity’s 2026 guidance recommends saving 15% of pre-tax income as a retirement benchmark, giving you a concrete target to anchor your plan. Managing financial anxiety means addressing both your account balances and your thought patterns. Neither alone is enough.

1. Build a realistic budget for clarity, not perfection

The single most effective first step in managing financial stress is building a budget that tells the truth about your money. AARP experts emphasize that clarity matters far more than perfection. A budget you actually use beats a flawless spreadsheet you abandon after two weeks.

Fidelity’s 60/30/10+15 framework offers a practical starting point. Allocate 60% of take-home pay to necessities, 30% to wants, 10% to short-term savings, and 15% of pre-tax income to retirement. That structure gives you permission to spend on wants without guilt, which is a powerful anxiety reducer on its own.

Starting simple is the key. Track your last 30 days of spending in three categories: needs, wants, and savings. You can refine from there. The goal is to replace vague dread with specific numbers you can actually work with.

- Write down every fixed expense (rent, utilities, subscriptions) before estimating variable costs.

- Use a budget that actually works by building in a small buffer for unexpected costs each month.

- Review your budget weekly for the first two months to catch surprises early.

- Adjust without judgment. Going over in one category is data, not failure.

Pro Tip: Set a 15-minute “budget check-in” every Sunday evening. Consistency matters more than duration.

2. Build an emergency fund as your financial circuit breaker

An emergency fund is the single best buffer between you and a debt spiral. Fidelity recommends keeping three to six months of essential expenses in an accessible account, such as a high-yield savings account or money market fund. For people with variable income, leaning toward six months provides extra cushion.

The fund only works if you protect it. Define “emergency” clearly before you need it. A car breakdown qualifies. A concert ticket does not. That boundary keeps the fund intact and keeps your anxiety lower because you know the money is actually there when you need it.

Starting small removes the psychological barrier. Even $500 in a dedicated account changes how you feel about an unexpected bill. That shift in feeling is real and measurable.

- Open a separate savings account specifically labeled “Emergency Fund” to reduce the temptation to spend it.

- Automate a fixed transfer on payday, even if it is only $25 per week to start.

- Pause contributions temporarily if you face a genuine emergency, then restart as soon as possible.

- Replenish immediately after any withdrawal so the fund stays at its target level.

Pro Tip: Treat your emergency fund contribution like a bill. Automate it so the decision is never left to willpower.

3. Use psychological techniques to quiet money anxiety

Financial anxiety has emotional roots that budgets alone cannot fix. Dr. Anne Browning recommends nature, gratitude, and social connection as daily tools to reset your nervous system when financial stress builds. These are not soft suggestions. They are evidence-based techniques that prevent stress from accumulating into overwhelm.

Graduated financial exposure is one of the most effective CBT-based tools for money anxiety. You start with the least threatening financial task, such as checking your bank balance, and work up to harder ones, like reviewing debt statements. Each completed task proves to your brain that the feared outcome did not happen. Over time, avoidance shrinks.

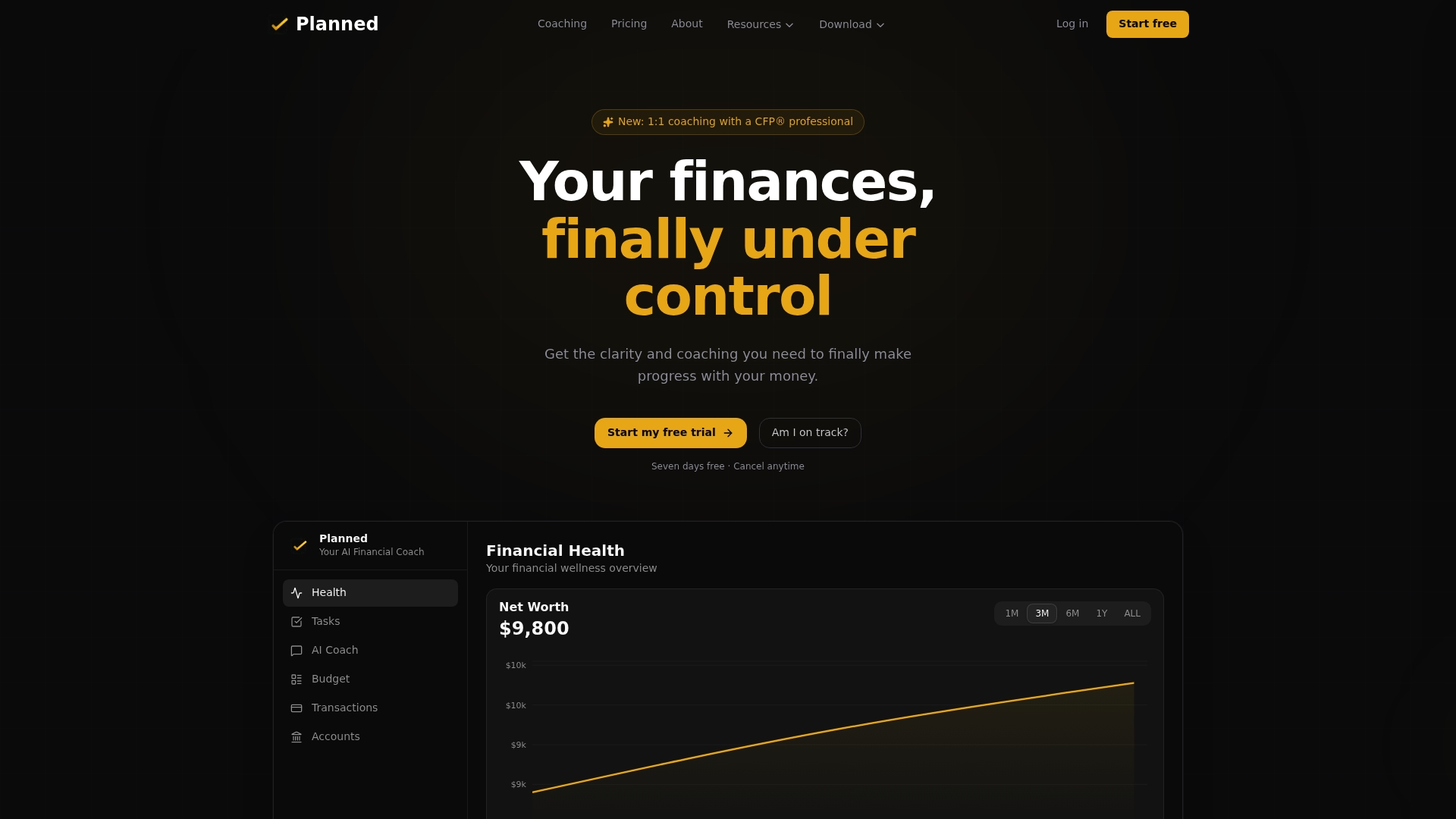

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Separating what you can control from what you cannot is equally powerful. You can control your savings rate. You cannot control a market correction. Focusing your energy on controllable actions reduces the helplessness that feeds anxiety.

“Financial anxiety cannot always be eliminated, but effective stress metabolization techniques can prevent overwhelm. Daily practices like gratitude, social connection, and time in nature help your nervous system process stress before it accumulates.” — Dr. Anne Browning, University of Washington Medicine

- Schedule a weekly “money time” session of 20–30 minutes to handle financial tasks. Containing worry to a set time prevents it from bleeding into the rest of your day.

- Practice a two-minute gratitude note after each money session to close the loop emotionally.

- Talk to one trusted person about your financial goals. Social accountability reduces shame and isolation.

- Separate “I can act on this” worries from “I cannot control this” worries in a simple two-column list.

4. Know when to seek professional support

Financial coaching and therapy serve different purposes, and knowing which one you need is itself a best practice for financial calm. These two approaches complement each other but do not substitute for each other.

| Support type | Primary focus | Best for |

|---|---|---|

| Financial coaching | Goal setting, behavior change, accountability | Building habits, creating plans, staying on track |

| Therapy (CBT) | Emotional healing, trauma, thought patterns | Chronic anxiety, avoidance, past money trauma |

| Combined approach | Both financial and emotional dimensions | Persistent anxiety with practical money challenges |

A financial coach helps you build a plan and stick to it. A therapist helps you understand why you sabotage the plan in the first place. Many people benefit from both at different stages. If you find yourself avoiding opening mail, losing sleep over money, or making impulsive financial decisions under stress, those are signals that professional support will accelerate your progress far more than another budgeting app.

Planned’s 1:1 financial coaching connects you with a CFP® professional who works from your actual account data, not generic templates. That specificity is what separates real coaching from generic advice.

5. Adopt daily habits that sustain financial wellness

Reducing financial anxiety over the long term requires consistent daily and weekly habits, not just one-time fixes. Quarterly financial reviews prevent small problems from becoming costly ones and build genuine confidence over time. Think of them as a 90-day check-up for your money health.

Daily habits matter just as much as scheduled reviews. Physical self-care directly supports financial decision-making. Sleep deprivation and poor nutrition impair the prefrontal cortex, which is the part of your brain responsible for planning and impulse control. Taking care of your body is a financial wellness strategy.

Avoiding obsession with short-term market movements is another underrated habit. Checking your investment account daily creates anxiety without improving outcomes. Weekly or monthly reviews are sufficient for most people.

- Track expenses weekly using a planner or free financial tools to stay aware without obsessing.

- Schedule a quarterly full financial review covering net worth, debt progress, savings rate, and upcoming large expenses.

- Prioritize 7–8 hours of sleep consistently. Fatigue makes financial decisions feel more threatening than they are.

- Limit investment account checks to once per week or less if market volatility triggers anxiety.

- Celebrate small wins. Paying off a credit card or hitting a savings milestone deserves acknowledgment.

6. Shift your money mindset to reduce avoidance

Avoidance is the most common and most damaging response to financial anxiety. When you avoid checking your balance or opening a bill, the anxiety does not go away. It compounds. The mindset and behavior shift from avoidance to curiosity is one of the most impactful changes you can make.

Reframing your financial situation as a problem to solve rather than a judgment of your worth removes a significant emotional barrier. Your net worth is not your self-worth. That distinction sounds simple, but it takes deliberate practice to internalize.

One concrete technique is the “five-minute rule.” Commit to looking at one financial statement for just five minutes. Most people find the anxiety peaks before they open it, not after. That experience, repeated enough times, rewires the fear response.

Connecting your financial goals to your personal values also sustains motivation. Saving for a home, a family trip, or early retirement feels different from saving because you “should.” Values-based goals survive the hard months when motivation fades.

Key Takeaways

The most effective approach to financial anxiety management combines a realistic budget, a funded emergency account, and consistent psychological practices that address both the numbers and the emotions behind them.

| Point | Details |

|---|---|

| Budget for clarity | Use Fidelity’s 60/30/10+15 framework as a starting point, not a rigid rule. |

| Fund your emergency account | Keep three to six months of essentials in a high-yield savings account. |

| Contain financial worry | Schedule weekly “money time” sessions to prevent anxiety from dominating daily life. |

| Match support to your need | Use financial coaching for behavior change and therapy for emotional roots. |

| Review quarterly | Scheduled full assessments every three months prevent small issues from growing. |

What I’ve learned about combining money plans with mindset work

Most financial advice treats anxiety as a side effect of bad money habits. My experience points the other way. The anxiety usually comes first, and the bad habits follow from it. Avoidance, impulsive spending, and paralysis around financial decisions are anxiety responses, not character flaws. Treating them as such changes everything about how you approach the fix.

The people I’ve seen make the most progress do two things simultaneously. They build a concrete financial structure, a budget, an emergency fund, a savings target, and they work on the thought patterns that made those things feel impossible before. Neither track alone produces lasting change. The structure without the mindset work collapses under stress. The mindset work without the structure has nothing to anchor it.

The hardest part to accept is that this takes time. You will not eliminate financial anxiety in a month. But you will reduce it measurably if you show up consistently. The goal is not a perfect financial life. The goal is a life where money stops being the thing that keeps you up at night.

Start with one habit from this list. Build from there. Patience with the process is not weakness. It is the actual strategy.

— Matt Schuberg

How Planned supports your financial wellness

Managing financial anxiety gets significantly easier when you have a clear picture of where you actually stand, not where you think you stand.

Planned connects an AI coach directly to your real financial accounts, so every insight is based on your actual income, spending, and goals. The Financial Health Score gives you an honest baseline in minutes. From there, Planned’s CFP® coaching provides personalized guidance on budgeting, debt, and savings strategies built around your specific situation. Early adopters consistently report feeling less anxious and more confident about their financial decisions. That combination of clarity and accountability is what makes the difference between knowing what to do and actually doing it.

FAQ

What are financial anxiety management best practices?

Financial anxiety management best practices combine structured financial planning, such as budgeting and emergency fund building, with psychological techniques like CBT and mindfulness to reduce money stress and improve decision-making.

How much should I save to reduce financial anxiety?

Fidelity recommends saving 15% of pre-tax income for retirement and maintaining three to six months of essential expenses in an emergency fund as core financial wellness benchmarks.

Does therapy help with money anxiety?

Yes. Therapy, especially CBT, targets the emotional roots of financial anxiety, including avoidance and catastrophic thinking. Financial coaching addresses goal setting and behavior change. Both serve distinct and complementary roles.

How do I stop obsessing over my finances?

Schedule a fixed weekly “money time” session of 20–30 minutes. Containing financial worry to a designated time reduces rumination and prevents anxiety from bleeding into the rest of your day.

What is the fastest way to feel less financially anxious?

Building even a small emergency fund, as little as $500, produces an immediate reduction in financial stress by creating a buffer between you and unexpected expenses. Pair that with a simple weekly budget review for compounding relief.

Recommended

Types of Personal Financial Goals: A Complete Guide

Personal financial goals come in short, medium, and long-term types, plus four function categories. See exactly how to prioritize and fund each in order.

Why Understanding Finances Reduces Fear and Anxiety

Understanding your finances reduces money anxiety by turning vague fears into concrete facts. Learn how financial literacy builds calm at any income level.

What Does Financial Profile Mean? Your 2026 Guide

Discover what a financial profile means and how it shapes your financial health. Learn to make smarter money decisions today!

How to Personalize Your Financial Plan by Income

Personalize your financial plan by income: total your real earnings, match your savings rate to your bracket, and review it quarterly as life changes.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?