How to Evaluate Major Life Financial Choices

Learn to evaluate major life financial choices wisely. Make informed decisions about investments, home buying, and more with our clear guide.

How to Evaluate Major Life Financial Choices

TL;DR:

- Major financial decisions should balance measurable data with personal values to ensure long-term success. Key choices like home buying, career changes, and investments determine most of your financial outcome, making careful evaluation essential. A structured process involving baseline assessment, opportunity cost analysis, qualitative projection, and regular reviews helps make these critical decisions effective and sustainable.

Evaluating major life financial choices means weighing measurable data against your personal values to reach decisions that hold up over time. The standard industry term for this process is financial decision evaluation, and it covers everything from buying a home to choosing between investing and paying off debt. A few key decisions carry outsized weight: getting big decisions right on partner choice, career path, spending philosophy, and major investments determines 95% of your financial outcome. That means your individual transactions matter far less than the handful of crossroads moments you face across a lifetime. This guide walks you through a clear, repeatable process for making those moments count.

How do you assess your financial health before a big decision?

Your financial baseline is the starting point for every major decision. Without it, you are comparing options without knowing what you can actually afford or absorb. A realistic baseline covers four areas: monthly income, fixed and variable expenses, outstanding debts, and current savings.

Start by mapping your cash flow. Cash flow analysis reveals liquidity and resilience beyond what income statements provide, and it enables scenario planning for shocks and growth. That matters because a decision that looks affordable on paper can collapse your finances if an unexpected expense hits six months later.

Use these checkpoints to define your decision boundaries:

- Net monthly surplus: What remains after all expenses and minimum debt payments. This number sets your realistic capacity for new financial commitments.

- Emergency fund status: A fund covering three to six months of expenses acts as a circuit breaker. Without it, a major decision carries far more risk.

- Debt-to-income ratio: Divide your total monthly debt payments by your gross monthly income. Lenders use 43% as a ceiling for mortgage qualification, and staying well below that gives you flexibility.

- Credit score range: This directly affects the interest rates available to you, which changes the true cost of any financed decision.

Pro Tip: Use Planned’s financial health assessment framework to score your baseline before comparing any options. Knowing your Financial Health Score removes the guesswork from what you can realistically take on.

Once you have a clear picture of your baseline, you can set firm boundaries. A home purchase might be realistic. A business investment might require six more months of saving first. The numbers tell you which conversation to have.

How do you quantify opportunity costs and compare financial alternatives?

Opportunity cost is the value of the best option you give up when you choose something else. It is the most underused concept in personal financial decision evaluation, and ignoring it leads to choices that feel right in the moment but cost you significantly over time.

The compounding effect makes opportunity cost dramatic at longer time horizons. A $5,000 vacation for a 25-year-old equates to $108,000 in future retirement purchasing power at an 8% return over 40 years. That is not an argument against vacations. It is an argument for knowing the real price of every spending decision before you make it.

For major decisions like buying versus renting, use these four steps to compare alternatives side by side:

- Calculate the price-to-rent ratio. Divide the home’s purchase price by the annual rent for a comparable property. A ratio below 15 generally favors buying, 15–20 is context-dependent, and above 20 favors renting. This single number reframes the entire buy-versus-rent debate.

- Model total ownership costs. Annual maintenance alone runs 1–2% of property value. Add property taxes, insurance, and HOA fees to get the true annual cost of ownership.

- Compare investment alternatives. House appreciation averages 3–4% annually, while the S&P 500 has historically returned about 10%. Over a 10-year period, that gap compounds into a significant difference in net worth.

- Apply risk-adjusted thinking. A higher expected return means nothing if the risk level would cause you to sell at the wrong time. Match the risk profile of each option to your actual risk tolerance, not your theoretical one.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

Pro Tip: Planned’s invest vs. pay off debt calculator runs this comparison using your real account data, so the output reflects your actual situation rather than a generic scenario.

The goal is not to find the mathematically perfect answer. The goal is to make the hidden costs visible so you can choose with full information.

When does the math not tell the whole story?

Numbers capture a lot, but they cannot capture everything. Transformative financial decisions reshape your identity and values, which means you need to evaluate the future version of yourself you want to become, not just your current preferences.

“Trying to quantify qualitative factors like love or lifestyle with numeric scales hides true trade-offs. Build a narrative to project and choose your future life story instead.” Making a big, life-changing decision? 7 steps to consider

This is where most financial frameworks fall short. A spreadsheet can tell you whether buying a home in a new city is affordable. It cannot tell you whether you will feel isolated there, whether the career opportunity is worth leaving your network, or whether the lifestyle fits who you are becoming.

Three techniques help you bring qualitative factors into the evaluation:

- Narrative projection. Write two short paragraphs: one describing your life two years after choosing Option A, and one describing your life after Option B. The version that feels more like you carries real information.

- The vanishing options test. Remove all current choices from the table and ask what you would do instead. This surfaces creative alternatives you may have overlooked, like renting for a year before buying, or taking a contract role before committing to a full career pivot.

- Values alignment check. List your top three personal values. Ask whether each option supports or conflicts with them. A financially optimal choice that conflicts with your core values tends to produce regret even when it succeeds on paper.

The point is not to let feelings override analysis. The point is to treat your values as real inputs, not afterthoughts. A decision that scores well on both the financial model and the narrative projection is the one you will commit to fully.

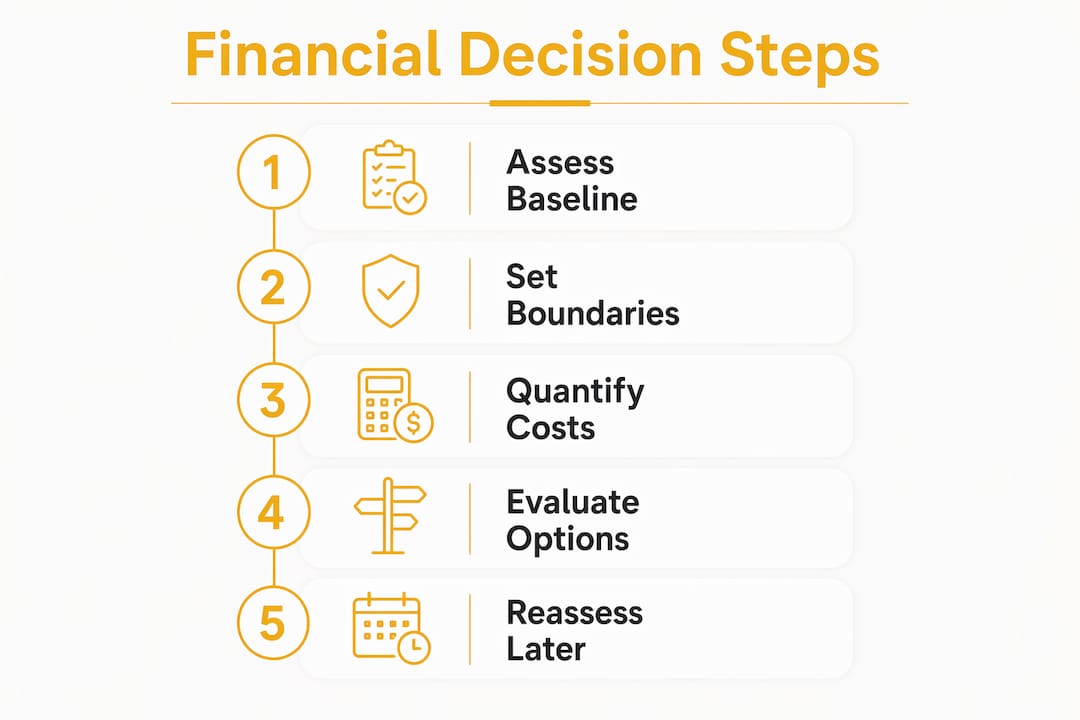

What is a clear process for making major financial decisions?

A repeatable process removes the paralysis that comes with high-stakes choices. Financial planning for life stages works best when you follow a sequence rather than jumping straight to a conclusion.

- Assess your baseline. Confirm your cash flow, emergency fund, debt load, and credit position before evaluating any option.

- Define your options broadly. Resist the two-option trap. Most decisions have at least three viable paths, including doing nothing for now.

- Quantify opportunity costs. Run the numbers on each option using real figures, not estimates.

- Project qualitatively. Use narrative projection and the values alignment check to evaluate what the numbers cannot measure.

- Stress test your choice. Run a premortem: assume the decision fails and work backward to identify why. Then run a backcast: assume it succeeds and identify what had to go right. Premortem and backcast visualization reveals key risks and success drivers while the decision is still reversible.

- Set a tripwire. Decide in advance what would cause you to revisit the decision. A tripwire prevents sunk cost thinking from locking you into a path that is no longer working.

Pro Tip: Schedule a formal reassessment at the six-month mark after any major financial commitment. Cash flow analysis at that point helps you catch stress points before they become crises.

Two common pitfalls derail this process. The first is impulsive commitment, where excitement about an option short-circuits the evaluation steps. The second is indefinite delay, where the fear of a wrong decision leads to no decision at all. Both carry real costs. Indecision is itself a choice, and it often has the highest opportunity cost of all.

Key Takeaways

Getting a handful of major financial decisions right matters far more than optimizing every small transaction, and the most reliable way to do that is combining financial analysis with honest qualitative reflection.

| Point | Details |

|---|---|

| Establish your baseline first | Know your cash flow, emergency fund, and debt-to-income ratio before evaluating any major option. |

| Quantify opportunity costs | Use the price-to-rent ratio, investment return comparisons, and total cost modeling to make hidden trade-offs visible. |

| Include qualitative factors | Narrative projection and the vanishing options test surface values and alternatives that numbers alone cannot capture. |

| Follow a repeatable sequence | Assess, compare, project, stress test, decide, and set a tripwire to avoid both impulsive and stagnant choices. |

| Reassess at set intervals | Schedule a formal review six months after any major commitment to catch problems while they are still manageable. |

The decisions that actually move the needle

I have spent years watching people agonize over small financial choices while sleepwalking through the big ones. Someone will spend three weeks researching the best high-yield savings account, then accept a job offer without negotiating salary. The math on that trade-off is not close.

The research backs this up. A handful of big decisions on career, partner, spending philosophy, and major investments shape the vast majority of your financial outcome. That is not a reason to be reckless with small decisions. It is a reason to reserve your deepest thinking for the moments that actually matter.

What I have found is that the people who make the best major financial decisions are not the ones with the most financial knowledge. They are the ones who know themselves well enough to recognize when a decision is primarily financial and when it is primarily about identity. Buying a home in a city you love is not just a real estate transaction. Leaving a stable career to start a business is not just a cash flow calculation. Treating these as purely financial problems produces technically correct answers that feel completely wrong.

My honest advice: do the math thoroughly, then ask whether the answer fits the life you are actually trying to build. If those two things align, commit fully. If they do not, keep looking. The worst outcome is not a suboptimal financial decision. The worst outcome is the right financial decision for the wrong life.

— Matt Schuberg

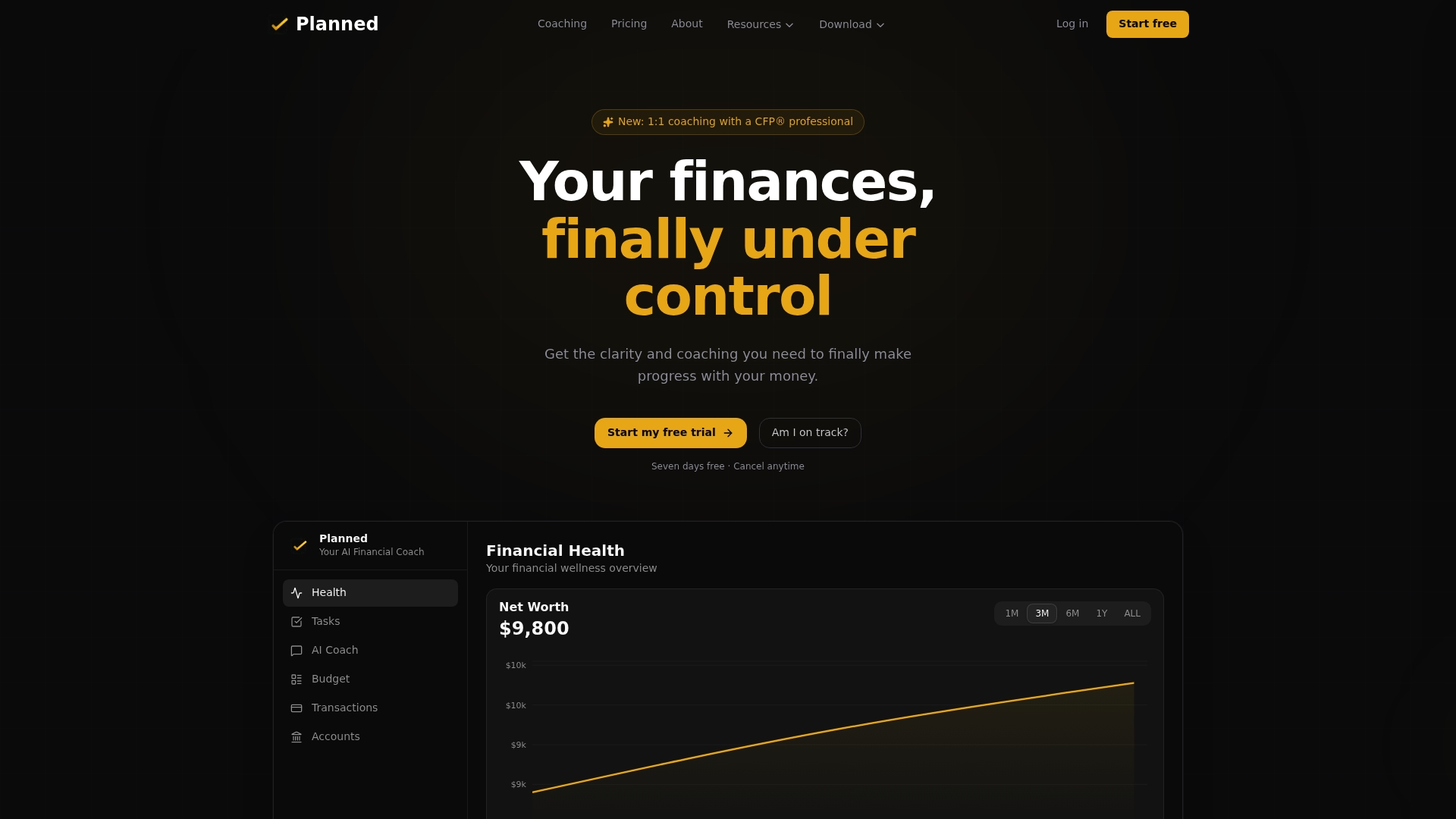

How Planned supports your biggest financial decisions

Major financial decisions carry real weight, and working through them with personalized guidance makes a measurable difference. Planned connects you with an AI coach linked directly to your real financial accounts, so the guidance you receive reflects your actual income, spending, and goals rather than generic assumptions.

Planned’s 1:1 financial coaching pairs you with a CFP® professional who can walk you through the full evaluation process, from baseline assessment to stress testing your final choice. Free tools like the invest vs. pay off debt calculator and the savings priority calculator let you model the numbers before your first coaching session. When you are standing at a crossroads, having the right tools and the right person in your corner changes the quality of the decision you make.

FAQ

What does it mean to evaluate major life financial choices?

Financial decision evaluation is the process of analyzing both quantitative factors, such as cash flow and opportunity cost, and qualitative factors, such as personal values and lifestyle fit, before committing to a significant financial path.

What is a good price-to-rent ratio for deciding whether to buy a home?

A price-to-rent ratio below 15 generally favors buying, while a ratio above 20 favors renting. Ratios between 15 and 20 require deeper analysis of your local market and personal situation.

How does opportunity cost affect major financial decisions?

Opportunity cost reveals the long-term value of the option you give up. A $5,000 spending decision today can represent over $100,000 in future purchasing power for a younger adult investing at historical market returns.

How do I factor in personal values when making a financial decision?

Use narrative projection to write out your life two years after each option, then check which scenario aligns with your top three personal values. This surfaces trade-offs that a spreadsheet cannot capture.

When should I reassess a major financial decision after making it?

Set a formal reassessment at the six-month mark. Running a cash flow analysis at that point helps you identify stress points early, while the decision is still adjustable rather than fully locked in.

Recommended

What Is Financial Confidence Building? A Clear Guide

Financial confidence building is the practice of managing money with awareness, structure, and consistent habits. Here's how to build it and cut money stress.

The Role of Small Wins in Finances: Build Real Wealth

Small financial wins are tiny, repeatable money habits that compound into real wealth. Here's the behavioral science, the math, and how to start today.

Financial Anxiety Management Best Practices That Work

Financial anxiety management works best when you pair a realistic budget and emergency fund with CBT techniques. Here's how to calm money stress that lasts.

Types of Personal Financial Goals: A Complete Guide

Personal financial goals come in short, medium, and long-term types, plus four function categories. See exactly how to prioritize and fund each in order.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?