The Financial Planning Process: A Step-by-Step Guide

Discover what is financial planning process with our step-by-step guide. Learn to assess your finances, set goals, and track progress effectively.

The Financial Planning Process: A Step-by-Step Guide

TL;DR:

- The financial planning process is a seven-step cycle that helps individuals set goals, build plans, and track progress. It is applicable at any income level and adapts to life changes, ensuring ongoing financial growth and stability. Regular updates after major life events optimize decision-making for budgeting, savings, and debt management.

The financial planning process is a structured, seven-step framework that guides you from understanding your current money situation to setting goals, building a plan, and tracking your progress over time. Certified Financial Planner (CFP®) professionals use this client-centered framework to deliver personalized guidance rather than one-size-fits-all advice. Whether you want to build a budget, grow your savings, or pay down debt, this process gives you a clear path forward. The best part: it works at any income level and any stage of life. Starting with a solid financial health assessment is the first real step toward feeling confident about your money.

What is the financial planning process?

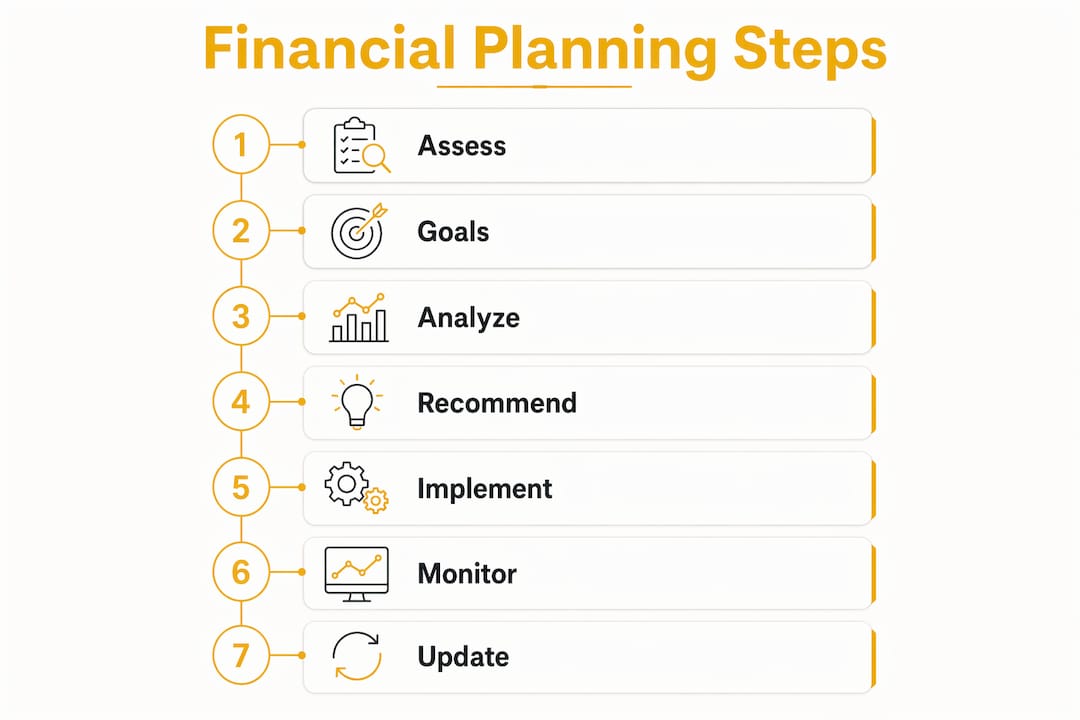

The financial planning process is a repeating cycle of seven steps that helps you make better money decisions over time. Each step builds on the last, and the process never truly ends. Life changes, and your plan needs to change with it.

Here are the seven steps, as defined by the CFP® standard:

-

Understand your personal and financial circumstances. Your planner (or you) gathers information about your income, expenses, debts, assets, family situation, and values. This step creates the foundation everything else rests on.

-

Identify and select your financial goals. You define what you want to achieve and by when. Goals might include buying a home, retiring at 60, or paying off student loans within five years.

-

Analyze your current actions and alternatives. This step examines what you are currently doing with your money and what other paths are available. It surfaces gaps between where you are and where you want to be.

-

Develop financial recommendations. Recommendations follow goal setting and analysis, not the other way around. A good plan aligns with your priorities before it ever suggests a specific product or account.

-

Present the recommendations. Your planner walks you through the options in plain language. You ask questions, push back, and decide what fits your life.

-

Implement the plan. This is where action happens. You open accounts, adjust contributions, set up automatic transfers, or pay down a specific debt.

-

Monitor progress and update the plan. A financial plan requires regular review, especially after major life events. This step keeps your plan relevant as your circumstances evolve.

Pro Tip: When reviewing recommendations in step four, ask whether each suggestion directly serves one of your stated goals. If it does not, it does not belong in your plan yet.

How does the financial planning process help with budgeting, saving, and debt?

Clear financial goals orient your spending priorities and guide every budgeting and saving decision you make. Without goals, a budget is just a list of numbers. With goals, it becomes a decision-making tool.

Here is how the planning process connects directly to the three areas most people care about most:

- Budgeting: Once your goals are set, you allocate your income to match them. If retiring early is the priority, more goes to savings. If paying off credit card debt is urgent, discretionary spending shrinks temporarily.

- Emergency fund: Emergency savings are a foundational part of any financial plan. Even a small buffer of $500 to $1,000 prevents you from reaching for a credit card when the car breaks down.

- Debt management: The plan identifies which debts carry the highest interest rates and builds a payoff sequence. Tackling high-interest debt first reduces the total amount you pay over time.

- Savings goals: Short-term goals (a vacation fund) and long-term goals (a down payment) each get their own savings bucket. Separating them makes progress visible and keeps you motivated.

- Resource allocation: As your income grows or expenses shift, the plan tells you where new money should go first. That prevents lifestyle inflation from quietly erasing your progress.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

A comprehensive financial plan covers budgeting, savings, debt, taxes, insurance, investments, and estate planning. That breadth matters because decisions in one area always affect the others. Paying off debt faster, for example, frees up cash that can then go toward retirement contributions.

Pro Tip: Use Planned’s invest vs. pay off debt calculator to see which move produces the better financial outcome for your specific situation before committing to either path.

Why is monitoring and updating your financial plan important?

A financial plan is not a document you write once and file away. Financial planning is recursive, meaning you continuously redefine goals and evaluate alternatives as your life evolves. That is not a flaw in the process. It is the point.

Life events are the main trigger for plan updates. The table below shows how common milestones change your financial picture and what needs to be reviewed as a result.

| Life event | What changes in your plan |

|---|---|

| Getting married | Combined income, shared goals, updated beneficiaries |

| Having a child | New savings goals, life insurance needs, education funding |

| Changing jobs | New income level, 401(k) rollover decisions, updated budget |

| Buying a home | Mortgage debt, property taxes, emergency fund size |

| Approaching retirement | Shift from growth to income, Social Security timing, withdrawal strategy |

Material life changes trigger plan reviews rather than fixed annual cycles. Waiting for a calendar date to review your plan means you might go months with a strategy that no longer fits your reality.

Periodic check-ins also prevent small drift from becoming a big problem. Spending creep, a raise you never redirected, or a debt you forgot to cancel after paying off can all quietly pull your plan off course. Knowing how to read your financial health report makes these check-ins faster and more useful.

Pro Tip: Set a calendar reminder to review your plan within 30 days of any major life event. Do not wait for the “right time.” The right time is right after the change happens.

Common challenges and misconceptions about financial planning

The biggest barrier to financial planning is not complexity. It is the belief that planning is only for people who already have money. Financial planning benefits everyone, regardless of income level, because it provides a strategy for reaching goals from wherever you currently stand.

Several other misconceptions keep people from starting:

- “Financial planning is just investing.” Investing is one piece of a much larger picture. A full financial plan also covers taxes, insurance, debt, and estate planning. Focusing only on investments while ignoring debt or insurance leaves serious gaps.

- “The process is too complicated for me.” The seven-step framework is designed to be worked through one step at a time. You do not need to solve everything at once. Starting with step one, understanding your current situation, is enough to build momentum.

- “I need to have my finances in order before I start.” This is backwards. The planning process exists precisely to help you bring order to a messy financial situation. You start where you are, not where you wish you were.

- “A financial plan means giving up everything fun.” A good plan reflects your values. If travel matters to you, your budget includes travel. The goal is alignment, not deprivation.

The CFP® framework is client-centered by design, meaning recommendations come from your goals, not from a product catalog. That distinction matters. A plan built around your priorities feels manageable. A plan built around product sales feels like a burden.

If you are not sure where to begin, reading about the 10 pillars of a financial plan gives you a concrete picture of what a complete plan actually covers.

Key Takeaways

The financial planning process is a seven-step, repeating cycle that connects your current financial situation to your long-term goals through budgeting, saving, debt management, and regular plan updates.

| Point | Details |

|---|---|

| Seven-step CFP® framework | The process moves from assessing circumstances to monitoring progress, in a continuous cycle. |

| Goals drive the budget | Clear financial goals tell you exactly where to direct your income each month. |

| Emergency fund first | A small emergency fund prevents debt from derailing your plan when unexpected costs hit. |

| Life events trigger reviews | Update your plan within 30 days of any major life change, not just once a year. |

| Planning is for everyone | The process works at any income level and starts from wherever you currently stand. |

Financial planning changed how I think about money

I have worked with people at every income level, and the pattern I see most often is this: the people who feel most anxious about money are usually the ones without a written plan, not the ones with the lowest incomes. That observation shifted how I think about what financial planning actually does.

A structured process does not just organize your money. It reduces the mental load of carrying every financial decision in your head. When you know your goals, your budget, and your next action, you stop second-guessing every purchase. That clarity is worth more than most people expect before they experience it.

The part most articles skip is that the monitoring step is where the real value compounds. Writing a plan is satisfying. Sticking to it through a job change, a new baby, or an unexpected medical bill is where the framework proves its worth. The people who revisit and adjust their plans consistently end up in a dramatically better position than those who treat planning as a one-time event.

My honest advice: do not wait until you feel “ready.” Start with step one, gather your numbers, and let the process do the work. The structure itself will tell you what to do next.

— Matt Schuberg

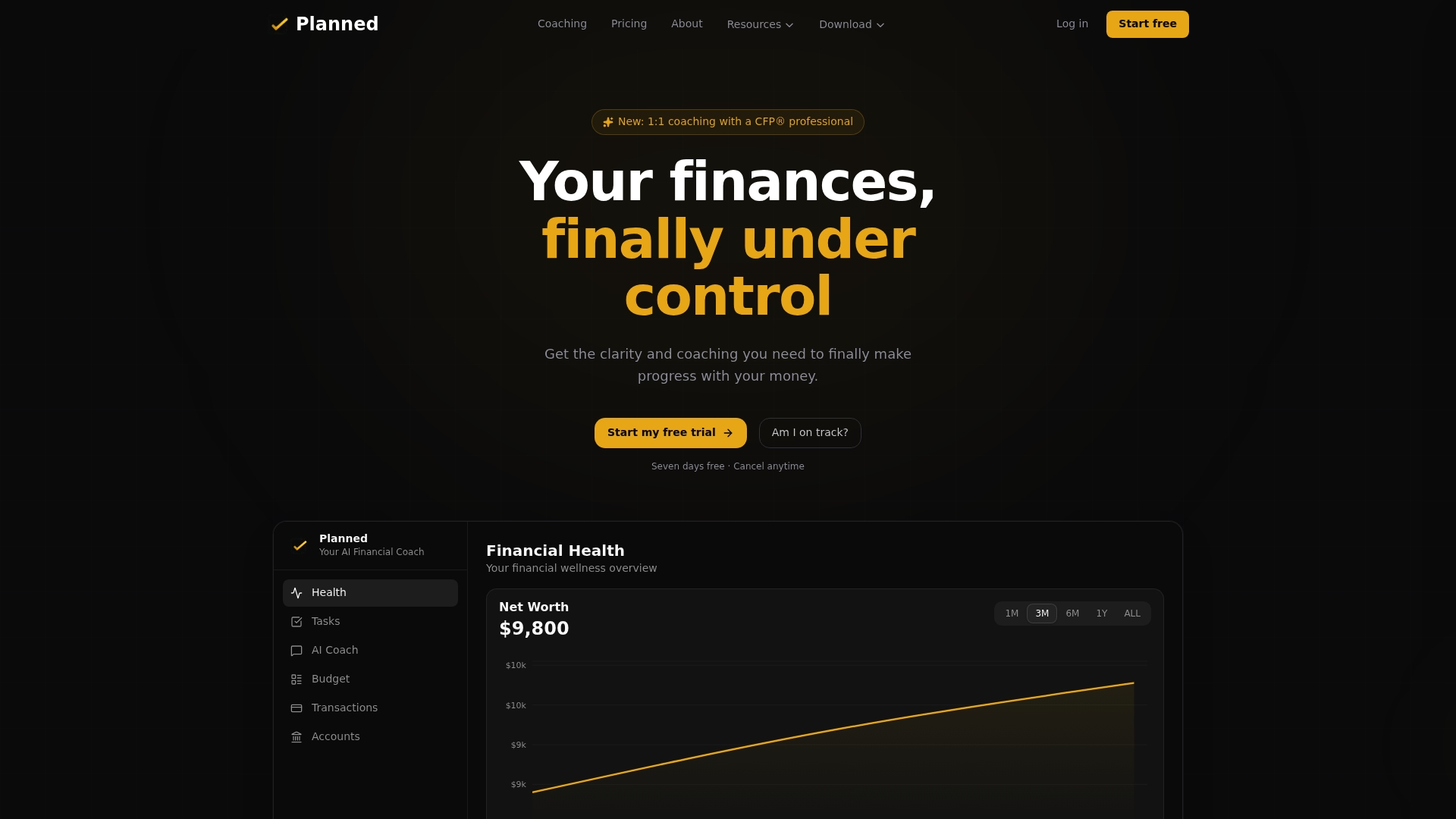

Planned makes the process personal

Getting a financial plan off the ground is easier when you have real guidance connected to your actual numbers, not generic advice that could apply to anyone.

Planned connects an AI coach directly to your financial accounts, so the guidance you receive reflects your real income, spending, and goals. Features like the Financial Health Score show you exactly where you stand and what to address first. For readers who want one-on-one support, CFP® coaching through Planned pairs you with a certified professional who builds recommendations around your priorities. Free financial tools including calculators for budgeting and debt decisions are available to anyone. Check Planned’s pricing to find the level of support that fits your situation.

FAQ

What is the financial planning process in simple terms?

The financial planning process is a seven-step framework that helps you assess your finances, set goals, build a plan, and monitor your progress over time. It is used by CFP® professionals and individuals alike to make better money decisions.

How many steps are in the financial planning process?

The CFP® standard defines seven steps, starting with understanding your circumstances and ending with monitoring and updating your plan on an ongoing basis.

Do I need a financial advisor to follow the financial planning process?

No. You can work through the steps on your own, especially with tools like budgeting calculators and financial health trackers. A CFP® professional adds value when your situation is complex or when accountability helps you stay on track.

How often should I update my financial plan?

Update your plan after any major life event such as a marriage, job change, or new child. Do not rely solely on a fixed annual review, since life rarely waits for a scheduled date.

Is financial planning only useful if I have a lot of money?

Financial planning benefits people at every income level. The process helps you build a strategy from your current situation, whether you are paying off debt, building an emergency fund, or saving for a first home.

Recommended

How to Optimize Finances Around Life Events

Optimizing finances around life events means adjusting your budget, savings, and insurance before and after milestones like marriage, a new job, or a baby.

Types of Personalized Financial Guidance: 2026 Guide

Personalized financial guidance includes credit counseling, CFP® professionals, coaching, and AI tools. Here's how to pick the right one for your money goals.

The Role of Financial Habits in Saving: Your Guide

Financial habits drive consistent saving by replacing willpower with automation. Build routines that make saving the default, even when money is tight.

How to Interpret Your Personal Finance Dashboard

A personal finance dashboard shows net worth, cash flow, and budget variances. Here's how to read each metric and turn the numbers into real decisions.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?