What Is Financial Mental Load and How to Manage It

Discover what is financial mental load and learn effective strategies to manage it. Take control of your finances and reduce stress today!

What Is Financial Mental Load and How to Manage It

TL;DR:

- Financial mental load is the ongoing cognitive effort of managing money, separate from active financial stress. It comprises tasks like tracking expenses and anticipating costs, which drain mental energy through constant low-level processing. Sharing financial clarity and automating payments can significantly reduce this invisible burden.

Financial mental load is the invisible, ongoing cognitive and emotional labor of tracking, anticipating, and managing your money, even when you are not actively making financial decisions. It is not the same as financial stress, which is a reaction to a specific problem like a surprise bill or job loss. Financial mental load is the chronic background hum of money thinking that never fully turns off. Nearly 75% of US adults named the economy as a significant stress source in 2026, and unmanaged household financial mental load makes that number worse. Understanding what financial mental load is gives you the first real tool to do something about it.

What is financial mental load, exactly?

Financial mental load is best understood as a form of cognitive labor, a term psychologists use to describe the mental work of managing life’s logistics. The standard industry term for this broader phenomenon is “cognitive load,” and financial mental load is its money-specific form. It includes remembering due dates, tracking subscriptions, mentally rehearsing “what if” scenarios, and anticipating future costs like insurance renewals or back-to-school expenses.

The key distinction is that financial mental load is driven by constant low-level mental processing, not by the act of paying bills itself. You can pay every bill on time and still feel exhausted because the real drain is the invisible inventory you carry in your head. Think of it as a browser with 30 tabs open. The tabs are not crashing your computer, but they are slowing everything else down.

This is different from the financial stress definition most people recognize. Financial stress is reactive. Financial mental load is chronic. One spikes when something goes wrong. The other runs quietly in the background every single day.

What tasks create and sustain this mental burden?

The specific tasks that build financial mental load are often mundane, which is exactly why they are so easy to underestimate. Each one feels small. Together, they create a significant drain on your mental energy.

| Money Task | Mental Load Component | Why It’s Draining |

|---|---|---|

| Tracking subscription renewals | Remembering dates and amounts | Requires constant vigilance with no clear endpoint |

| Budgeting in real time | Comparing spending to goals mid-month | Forces ongoing mental math and self-monitoring |

| Anticipating future costs | Projecting childcare, insurance, repairs | Creates “what if” loops that occupy background thinking |

| Managing multiple accounts | Monitoring balances across platforms | Grows harder as financial complexity increases |

| Remembering bill due dates | Mental calendar management | Failure carries real consequences, raising stakes |

The difference between active money actions and mental storage is critical. Paying a bill takes five minutes. Remembering that the bill is coming, worrying about whether the balance will cover it, and mentally flagging it for the next two weeks takes far more energy. That mental storage is where the real burden lives.

Pro Tip: Write down every recurring financial task you currently hold in your head, including amounts, due dates, and login details. Externalizing this “invisible inventory” onto paper or a personal finance dashboard immediately reduces the cognitive weight you carry.

Who carries the most financial mental load?

The burden of financial mental load is not distributed equally. Research consistently shows that women carry a disproportionate share of what some researchers call the “third shift” of financial cognitive labor, on top of paid work and household responsibilities. This load includes anticipating costs like childcare and insurance renewals that often go unacknowledged as real work.

How does my money actually stack up?

Most people feel behind financially but have no idea where they actually stand.

The consequences are measurable. Research from 2024 links this disproportionate financial cognitive labor to:

- Greater emotional exhaustion and fatigue

- A stronger desire to leave jobs or reduce work hours

- Reduced relationship satisfaction when the load is invisible to a partner

- Increased anxiety tied to financial decision-making

“Systems often get outdated as financial complexity grows, causing avoidable stress.” — Wealth advisor Kara Duckworth

Duckworth’s observation points to something important: the problem is not personal failure. Financial complexity often outpaces the systems people build to manage it. A spreadsheet that worked at 25 may collapse under the weight of a mortgage, a retirement account, a side income, and two kids’ college savings at 35. The load grows, but the system stays the same.

Household dynamics also matter. When one partner owns all financial administration, the other partner loses financial literacy over time. That imbalance creates both a mental load problem and a financial vulnerability problem.

How does financial mental load affect your well-being and decisions?

Carrying a high financial mental load does real psychological damage over time. Financial anxiety results in persistent negative thoughts and chronic worry that erode quality of life. In severe cases, the effects mirror PTSD-like symptoms, including hypervigilance, avoidance, and emotional numbness around money topics.

The behavioral effects are just as significant:

- Scarcity thinking: Constant money worry narrows your focus, making it harder to think creatively or plan long-term.

- Decision fatigue: After mentally managing finances all day, even small choices like whether to buy coffee feel harder than they should.

- Avoidance: Some people stop opening bank apps or checking balances entirely because the anxiety is too high.

- Impulsivity: Others make quick purchases to get temporary relief from the pressure of constant financial vigilance.

“Financial mental load creates a background anxiety that leaks into every area of life, affecting sleep, relationships, and the ability to be present.” — Digital Wellness Journal

The effects of financial stress do not stay in the money category. They show up in your sleep quality, your patience with people you love, and your ability to focus at work. Understanding financial burden means recognizing that it is a whole-life issue, not just a money issue. If you recognize these patterns in yourself, reading about financial anxiety in your late 20s can help you see you are not alone.

How to manage financial mental load effectively

Reducing financial mental load does not require a complete financial overhaul. That approach usually backfires. Gradual system implementation prevents overload and the abandonment of new habits. Start with one change, let it stick, then add the next.

Here are the most effective strategies, ordered by impact and ease:

-

Automate recurring payments and savings. Set up automatic transfers for bills, savings contributions, and debt payments. Automation of recurring bills is the most effective low-effort strategy for reducing financial mental load. When a task no longer requires your attention, it stops occupying mental space.

-

Schedule a weekly money date. Set aside 20–30 minutes once a week to review your finances. This creates a boundary. Instead of thinking about money all week, you contain it to one focused session. Outside that window, you give yourself permission to let it go.

-

Build shared clarity with your partner. Shared clarity means both partners can confidently answer basic financial questions: What is our monthly spending? When does the car insurance renew? What are our savings goals? True relief requires both people equally informed, not just one person reporting to the other.

-

Externalize your financial inventory. Move everything out of your head and into a system. A simple spreadsheet, a notes app, or a free financial tool works. The goal is to stop using your brain as a filing cabinet.

-

Work with a financial coach. A professional can help you build systems, prioritize goals, and offload the planning effort entirely. This is especially useful when your finances have grown more complex than your current system can handle.

Pro Tip: Build strong financial habits one at a time. Automate one bill this week. Schedule your first money date next week. Small wins compound into lasting relief.

Key takeaways

Financial mental load is a chronic cognitive burden that requires deliberate system design to reduce, not willpower or better memory.

| Point | Details |

|---|---|

| Definition matters | Financial mental load is chronic background money thinking, distinct from reactive financial stress. |

| The invisible inventory drains you | Remembering due dates and anticipating costs costs more energy than paying bills. |

| Load is unevenly distributed | Women and sole financial managers in households carry a disproportionate cognitive burden. |

| Emotional impact is real | Chronic financial mental load leads to anxiety, decision fatigue, avoidance, and impulsivity. |

| Automation is the fastest fix | Automating bills and savings removes tasks from your mental queue with minimal effort. |

The part most financial advice skips

I have noticed that most financial content focuses on what to do with your money. Very little of it addresses the cost of thinking about your money. That gap is where a lot of people quietly suffer.

The most useful shift I have seen is when someone stops treating their financial mental load as a personal failing and starts treating it as a design problem. Your brain was not built to track 14 subscriptions, 3 savings goals, a mortgage, and a retirement account simultaneously. No one’s brain was. The problem is not you. The problem is that you have not yet built a system that matches the complexity of your financial life.

Shared clarity, as wealth manager Andrew Woodward describes it, is the goal worth aiming for in any household. Not one person managing everything and occasionally briefing the other. Both people knowing enough to act independently. That shift alone removes an enormous amount of invisible labor from whoever has been carrying it alone.

CFP Matt Sheers points to mindfulness and gratitude practices as tools for breaking negative financial thought cycles. I would add one practical layer: you cannot be mindful about money if you are drowning in financial mental clutter. The mindset work and the system work have to happen together. Build the system first. The mental space follows.

— Matt Schuberg

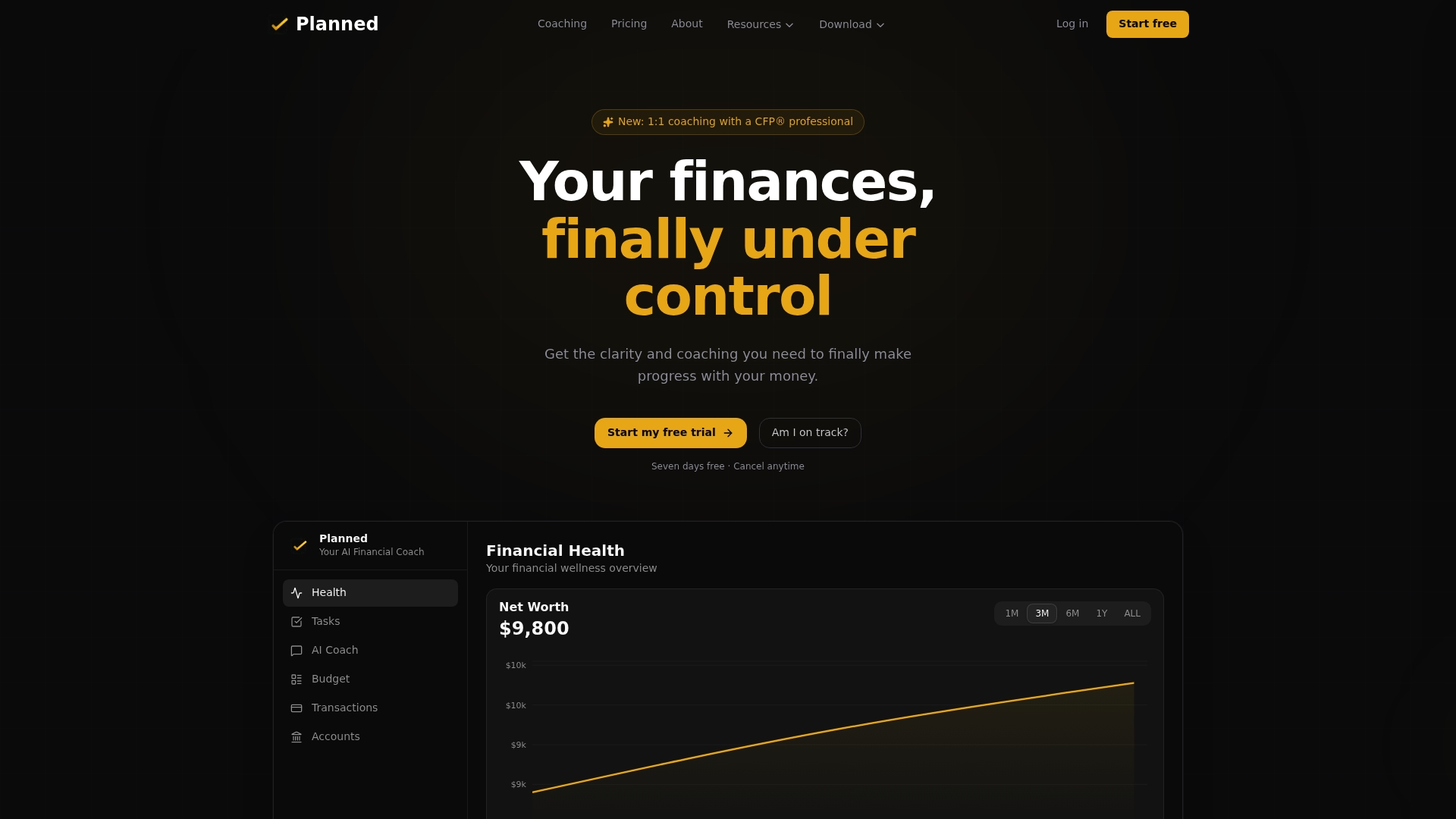

Planned: a financial coach that carries some of the load with you

Managing financial mental load is easier when you have a real system and real support behind you.

Planned connects you with 1:1 coaching from a CFP® professional who helps you build the exact systems that remove money tasks from your mental queue. Instead of generic advice, Planned’s AI coach connects directly to your real financial accounts and gives you answers based on your actual income, spending, and goals. Features like the Financial Health Score show you exactly where you stand, so you spend less time worrying and more time acting. Early adopters report reduced financial anxiety and greater confidence in their decisions. If you are ready to stop carrying your finances entirely in your head, Planned is built for that.

FAQ

What is financial mental load in simple terms?

Financial mental load is the ongoing mental work of tracking, anticipating, and managing money, even when you are not actively making transactions. It is the invisible cognitive labor that runs in the background of daily life.

How is financial mental load different from financial stress?

Financial stress is a reaction to a specific problem, like a missed payment or job loss. Financial mental load is a chronic, low-level cognitive burden that persists regardless of whether anything is currently going wrong.

Who is most affected by financial mental load?

Women disproportionately carry financial mental load due to social roles and household dynamics. Research from 2024 links this burden to greater emotional exhaustion and a stronger desire to reduce work hours.

What is the fastest way to reduce financial mental load?

Automating recurring bills and savings contributions is the most effective low-effort strategy. It removes tasks from your mental queue without requiring ongoing attention or willpower.

Can financial mental load affect my relationship?

Yes. When one partner carries all financial administration, the other loses financial literacy over time. Shared clarity, where both partners can answer key financial questions confidently, significantly reduces mental load and improves relationship safety.

Recommended

Why Financial Goals Need Tracking to Actually Work

Tracking financial goals is what turns intention into real results. See which metrics matter, how often to review, and how to build a habit that sticks.

The Financial Planning Process: A Step-by-Step Guide

The financial planning process is a seven-step cycle to set goals, budget, save, and pay off debt. Here's how each step works and where to begin today.

How to Optimize Finances Around Life Events

Optimizing finances around life events means adjusting your budget, savings, and insurance before and after milestones like marriage, a new job, or a baby.

Types of Personalized Financial Guidance: 2026 Guide

Personalized financial guidance includes credit counseling, CFP® professionals, coaching, and AI tools. Here's how to pick the right one for your money goals.

See my financial health score.

Most people feel behind but have no idea where they actually stand. Score yourself across all 10 areas in 2 minutes.

Am I on track?